Linear Regression

A Brief Review

About me

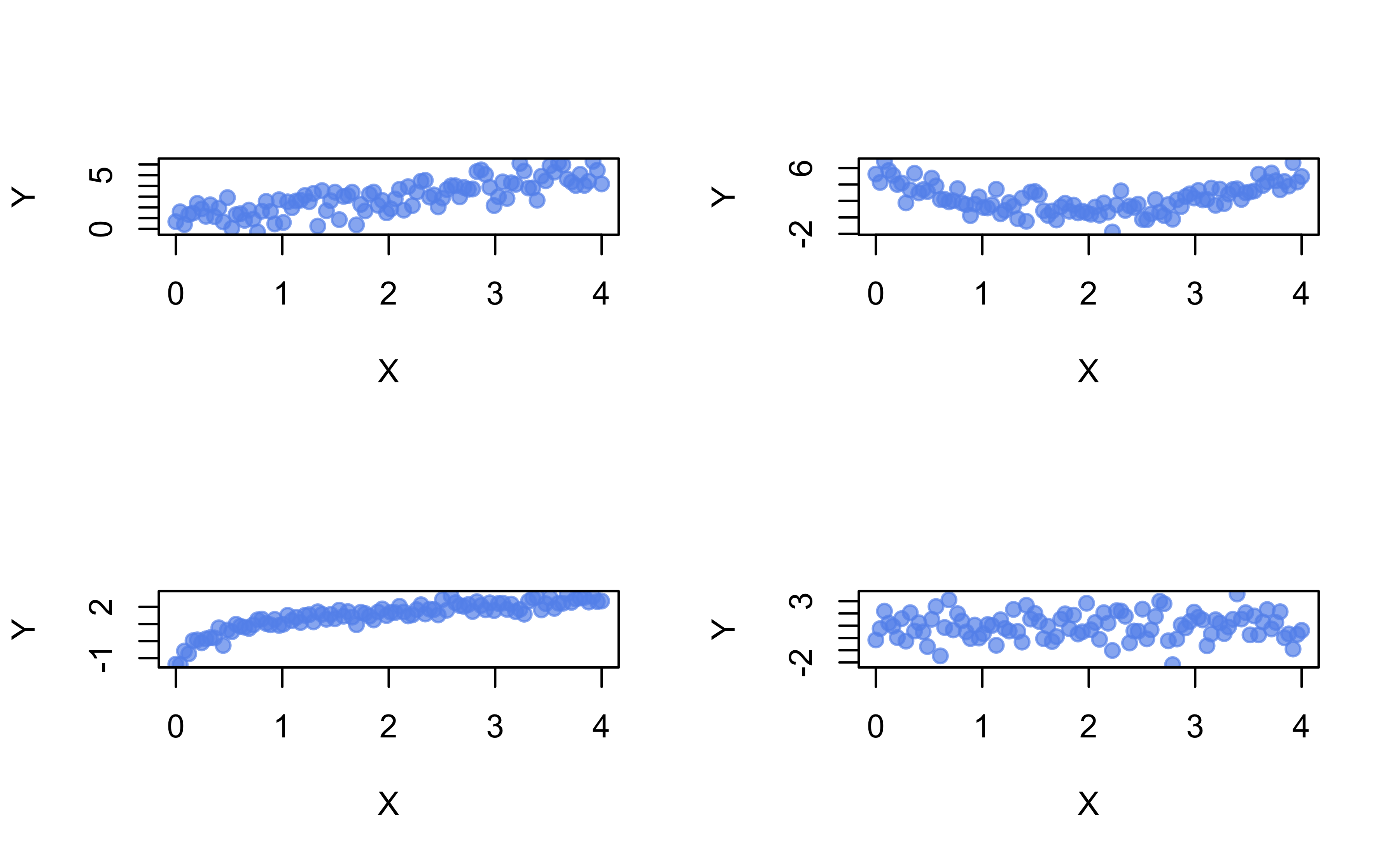

Statistical relationships

Show R code

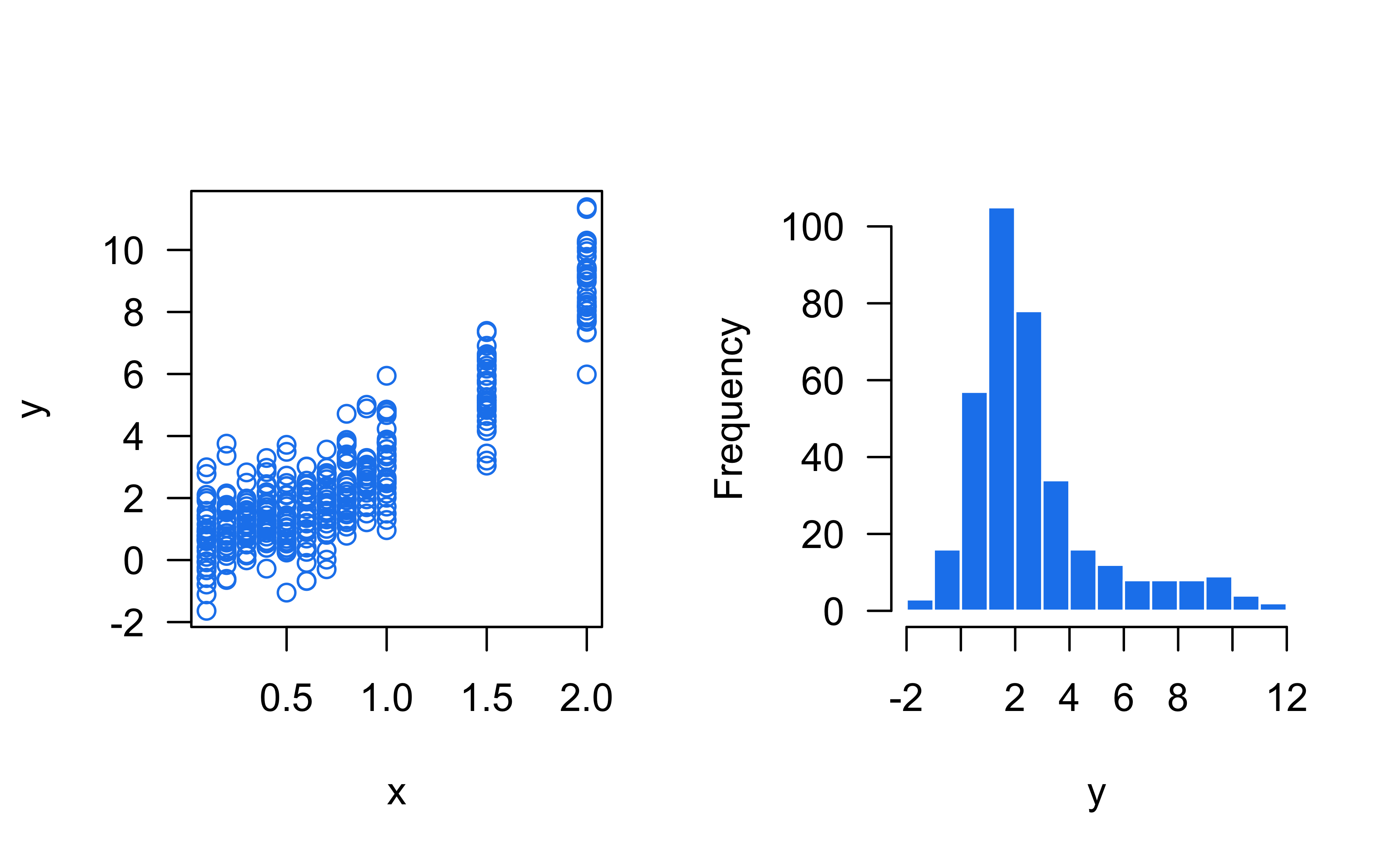

# Simulate data from different SLR models

set.seed(101) # for reproducibility

x <- seq(from = 0, to = 4, length = 100)

y <- cbind(

1 + x + rnorm(length(x)), # linear

1 + (x - 2)^2 + rnorm(length(x)), # quadratic

1 + log(x + 0.1) + rnorm(length(x), sd = 0.3), # logarithmic

1 + rnorm(length(x)) # no association

)

# Scatterplot of X vs. each Y in a 2-by-2 grid

par(mfrow = c(2, 2))

for (i in 1:4) {

plot(x, y[, i], col = adjustcolor("cornflowerblue", alpha.f = 0.7),

pch = 19, xlab = "X", ylab = "Y")

}

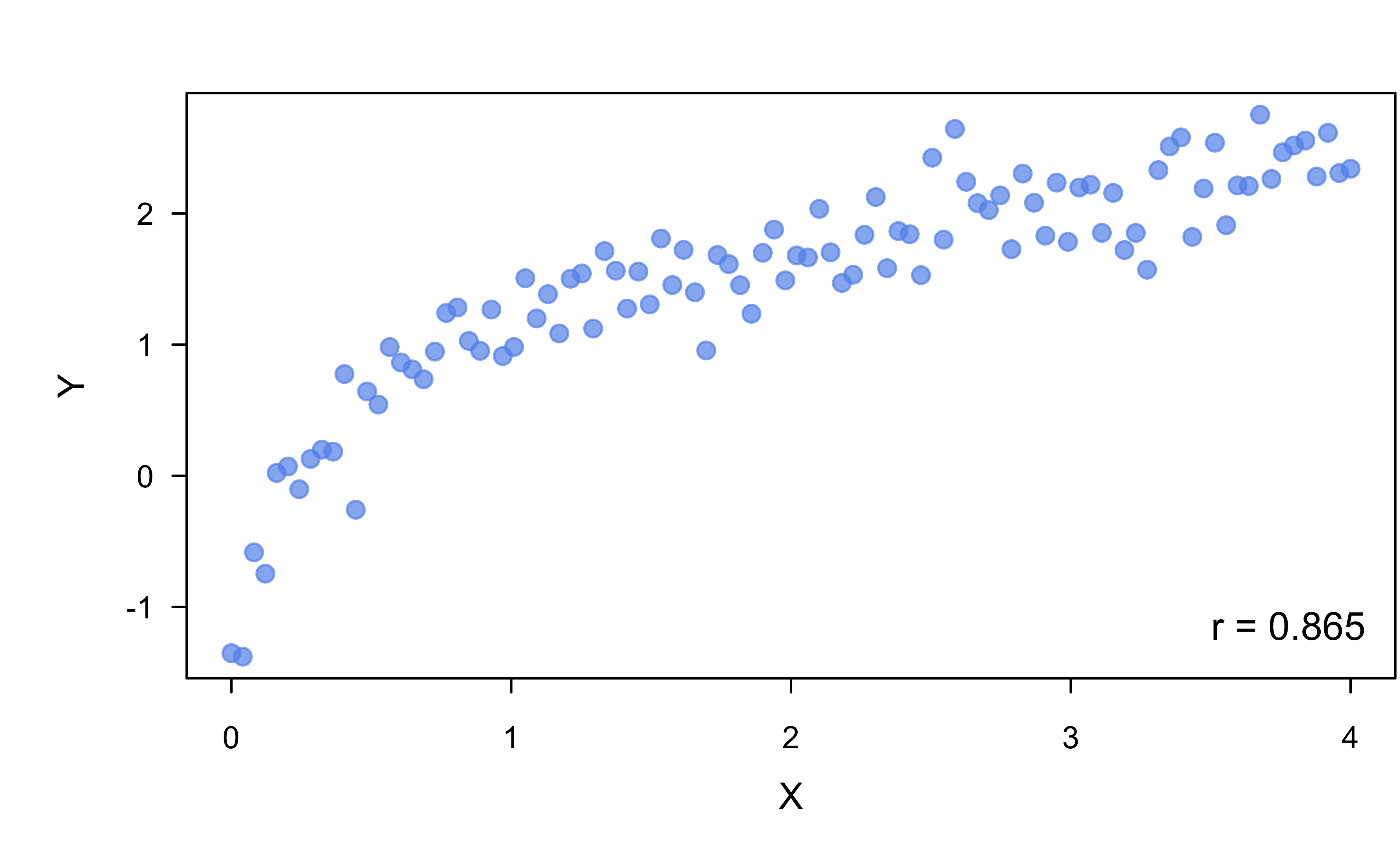

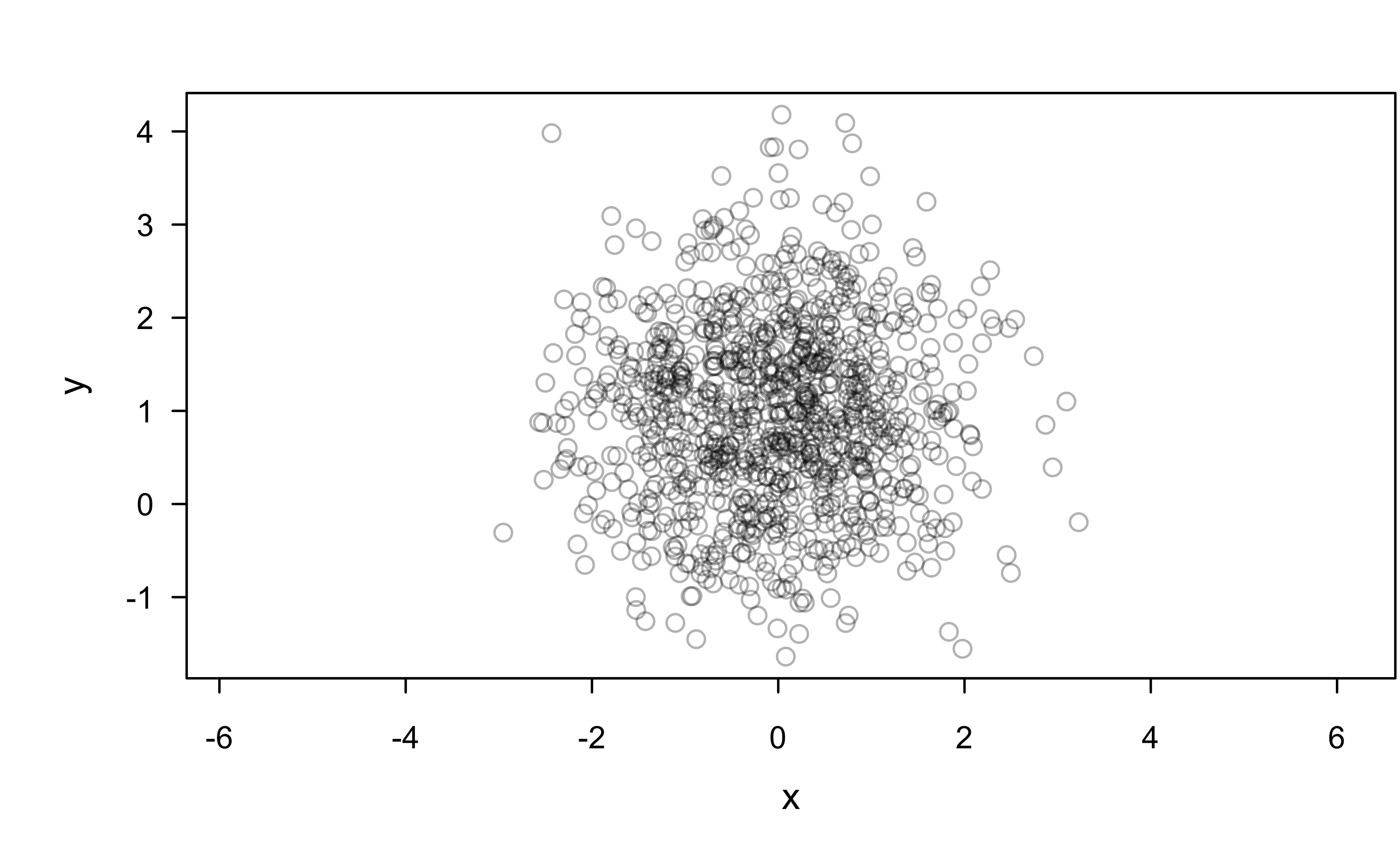

Are \(X\) and \(Y\) correlated?

Are \(x\) and \(y\) correlated?

All models are wrong!

Also, see this talk by my old adviser, Thad Tarpey: “All Models are Right… most are useless.”

Statistical relationships

Show R code

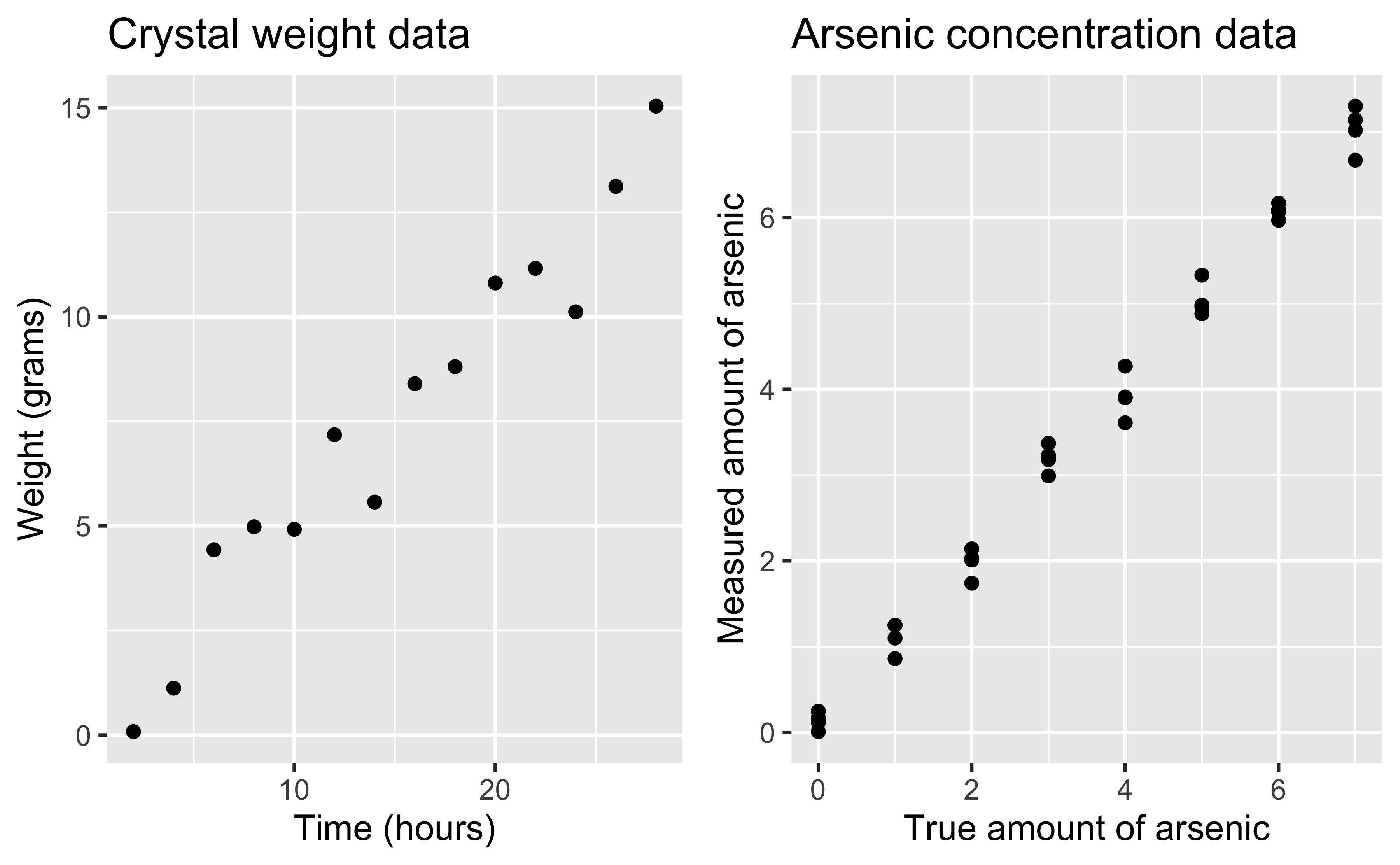

library(ggplot2)

p1 <- ggplot(investr::crystal, aes(x = time, y = weight)) +

geom_point() +

labs(x = "Time (hours)",

y = "Weight (grams)",

title = "Crystal weight data")

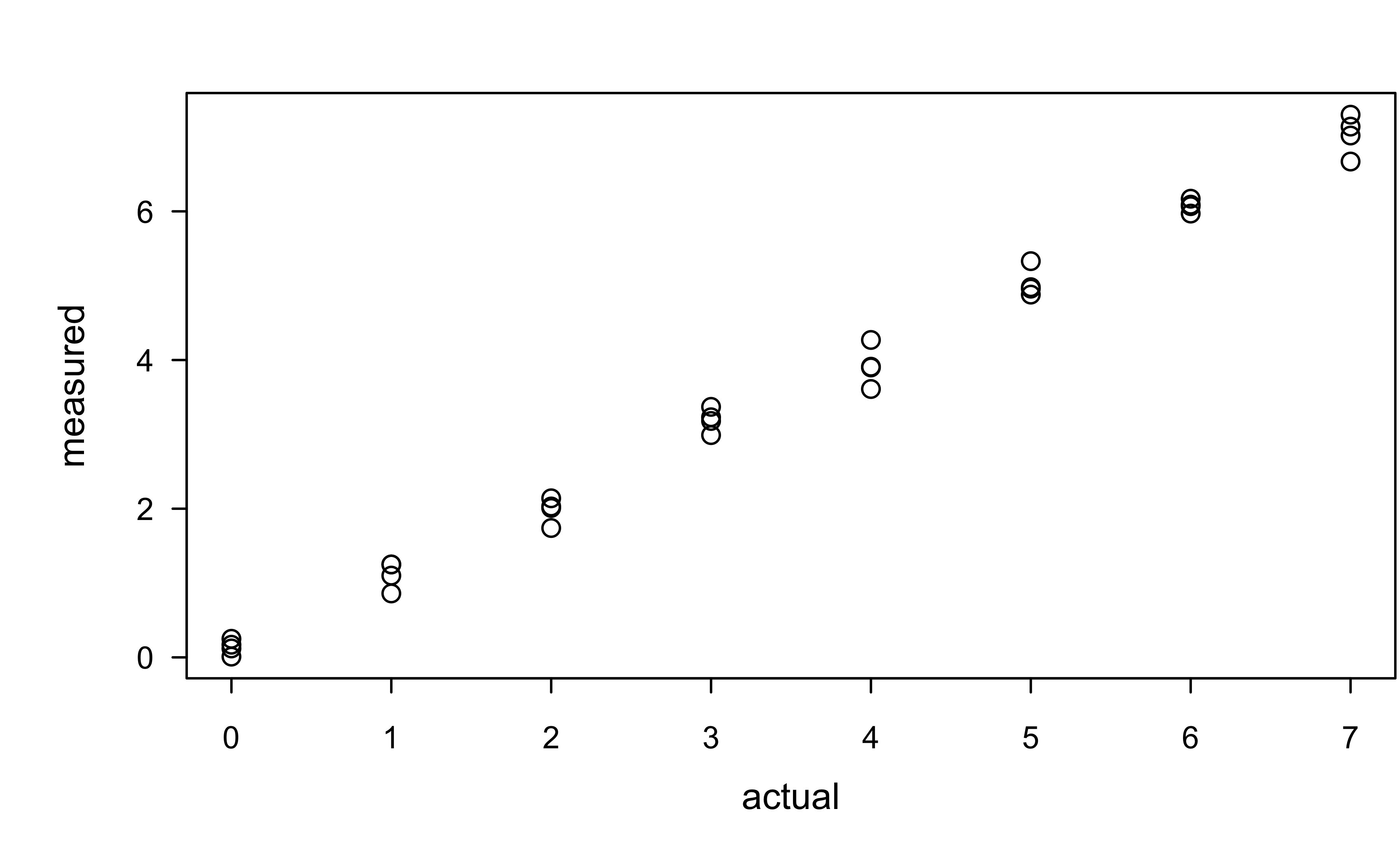

p2 <- ggplot(investr::arsenic, aes(x = actual, y = measured)) +

geom_point() +

labs(x = "True amount of arsenic",

y = "Measured amount of arsenic",

title = "Arsenic concentration data")

gridExtra::grid.arrange(p1, p2, nrow = 1)

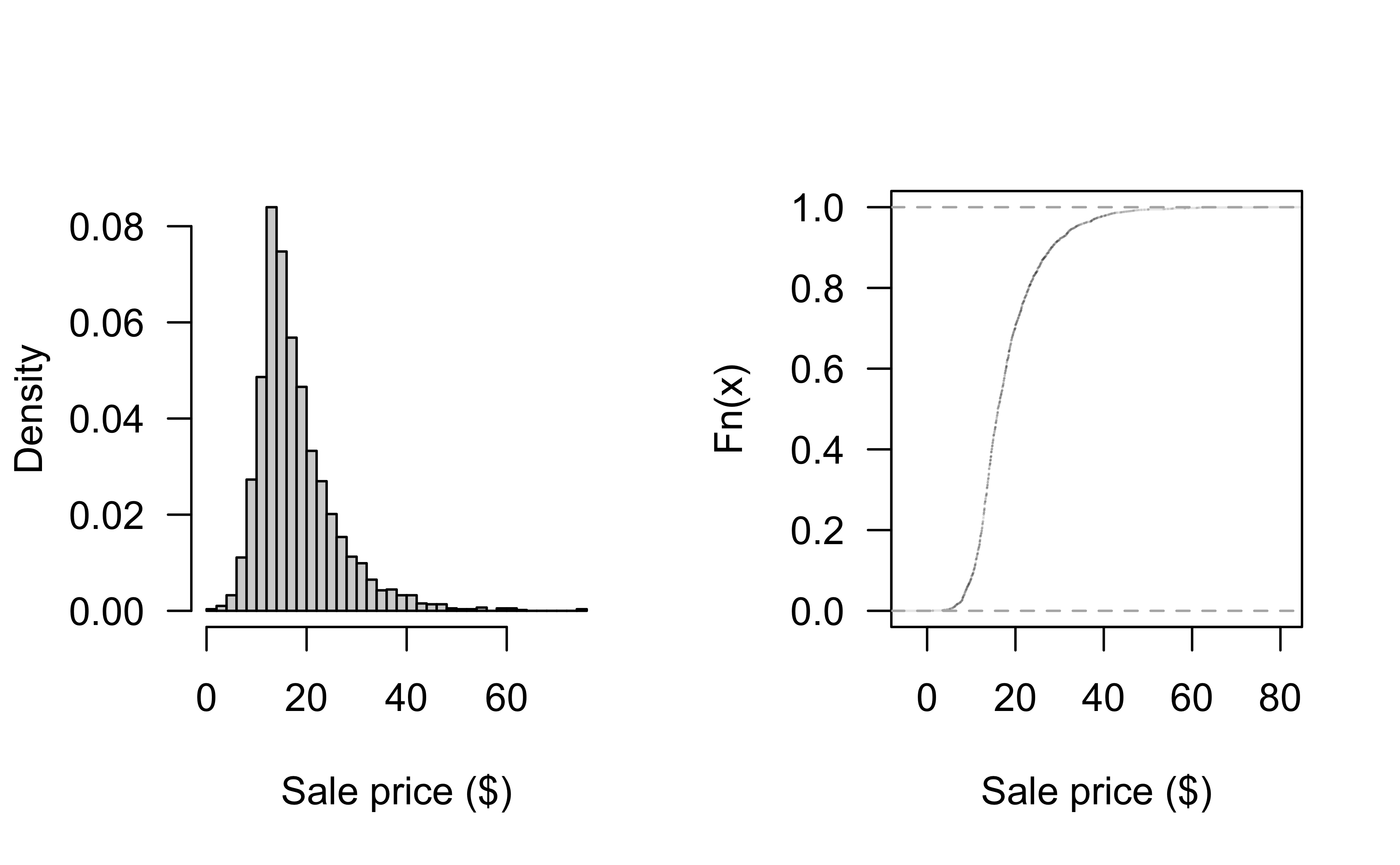

Distribution of Sale_Price

Can look at historgram and empirical CDF:

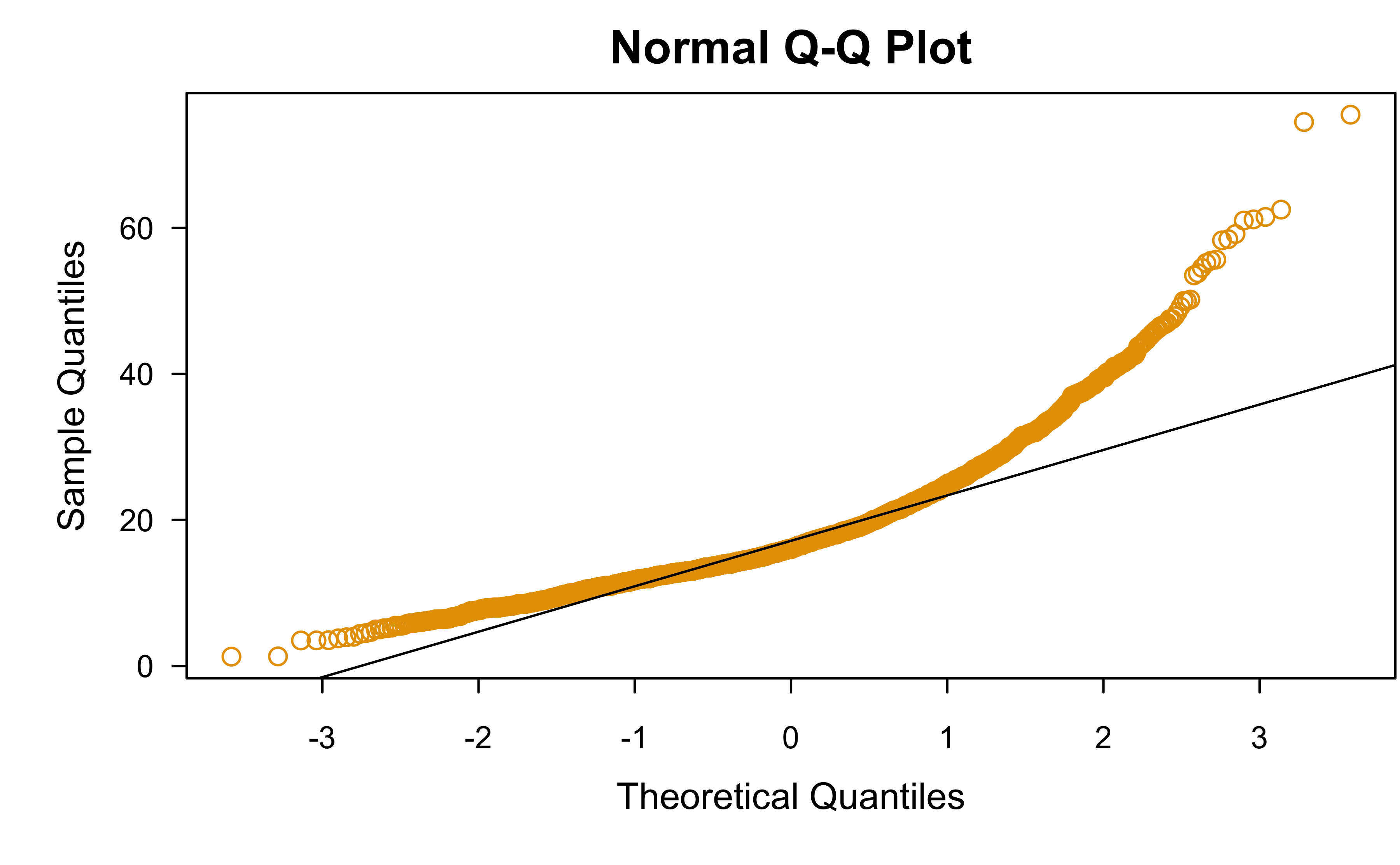

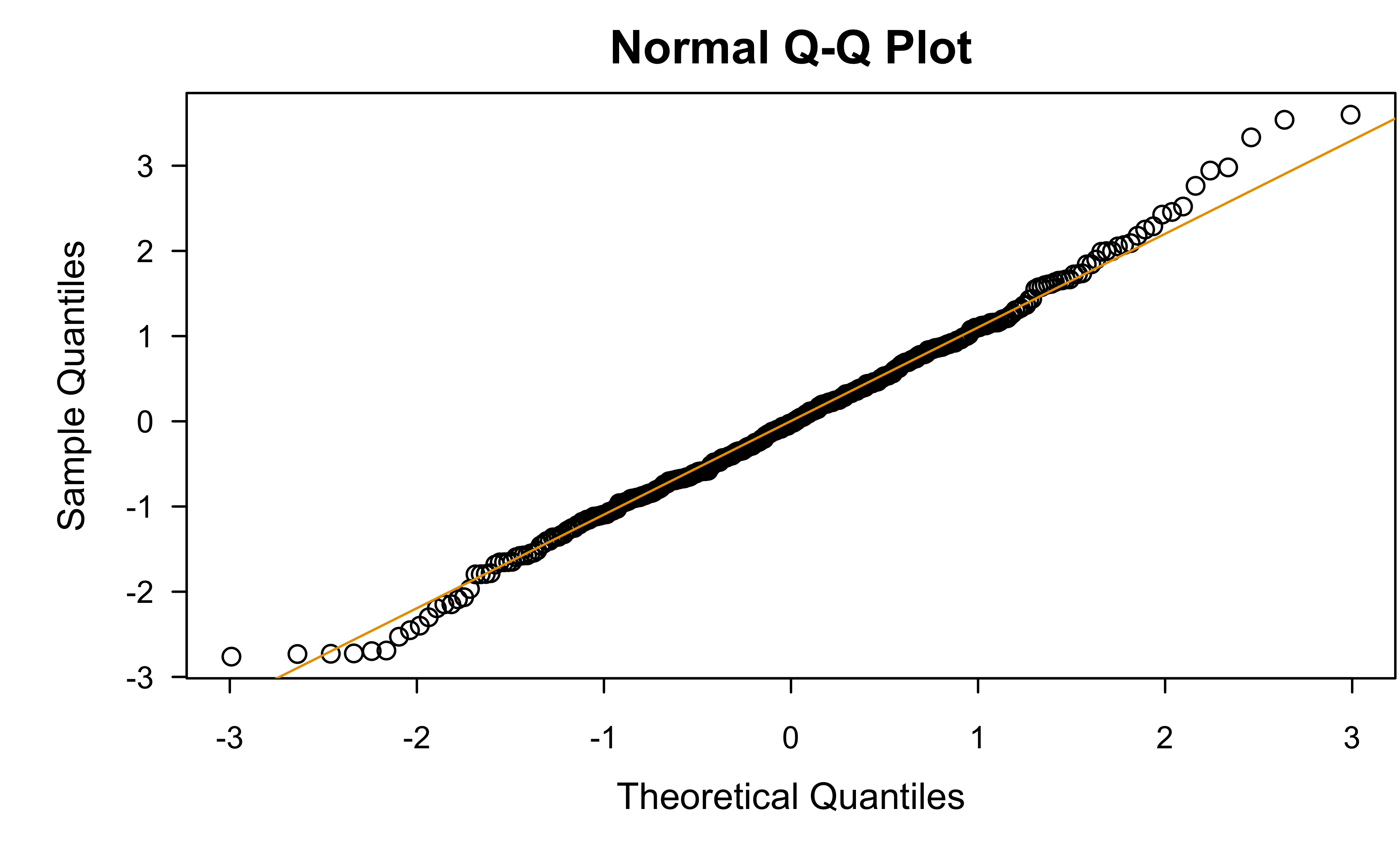

Normal QQ plot

Normal quantile-quantile (Q-Q) plot* can be used to asses the “normalityness” of a set of observations

Q-Q plots can, in general, be used to compare data with any distribution!

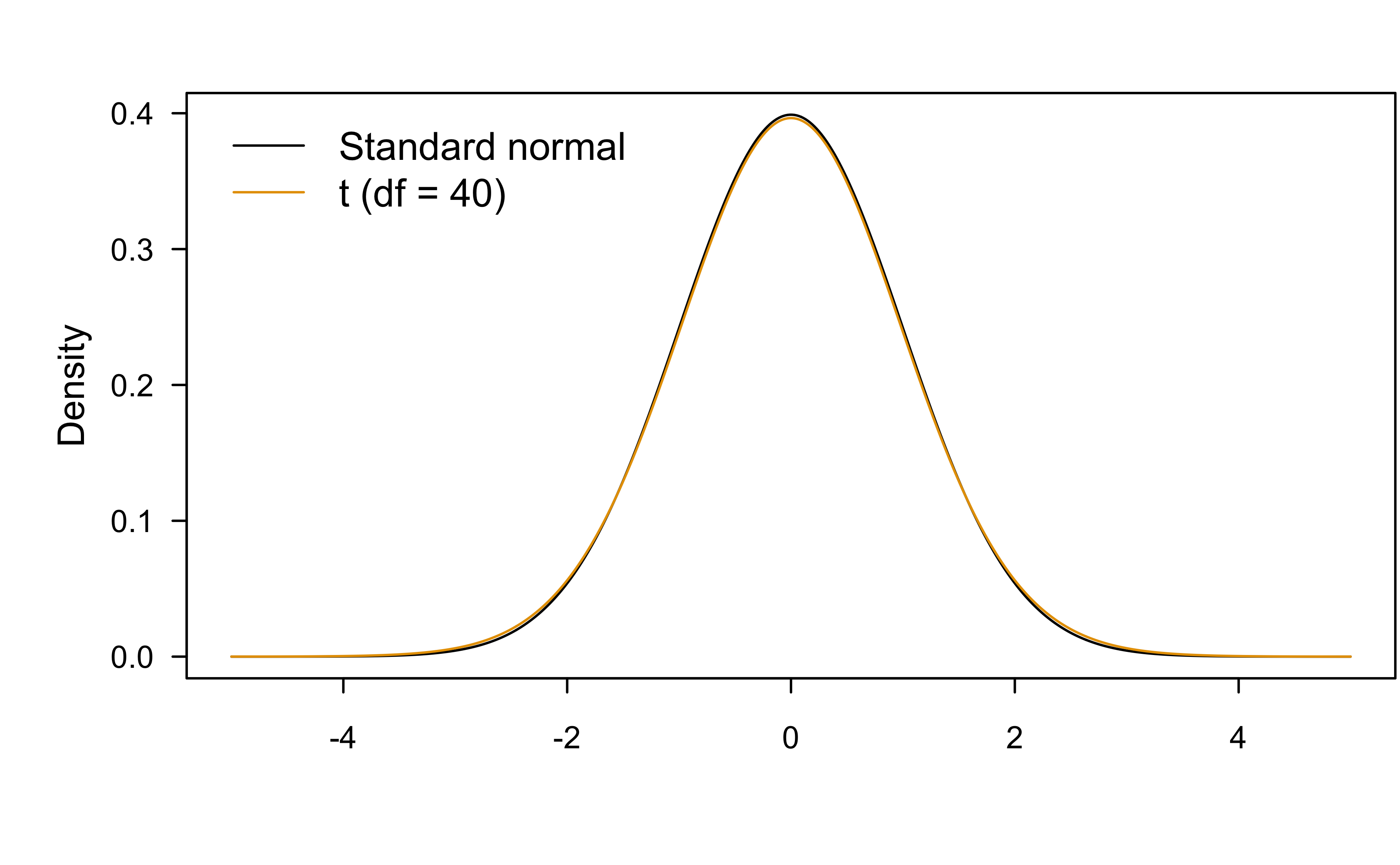

Normality tests 🤮

Are these two distributions significantly different?

Are these two distributions practically different?

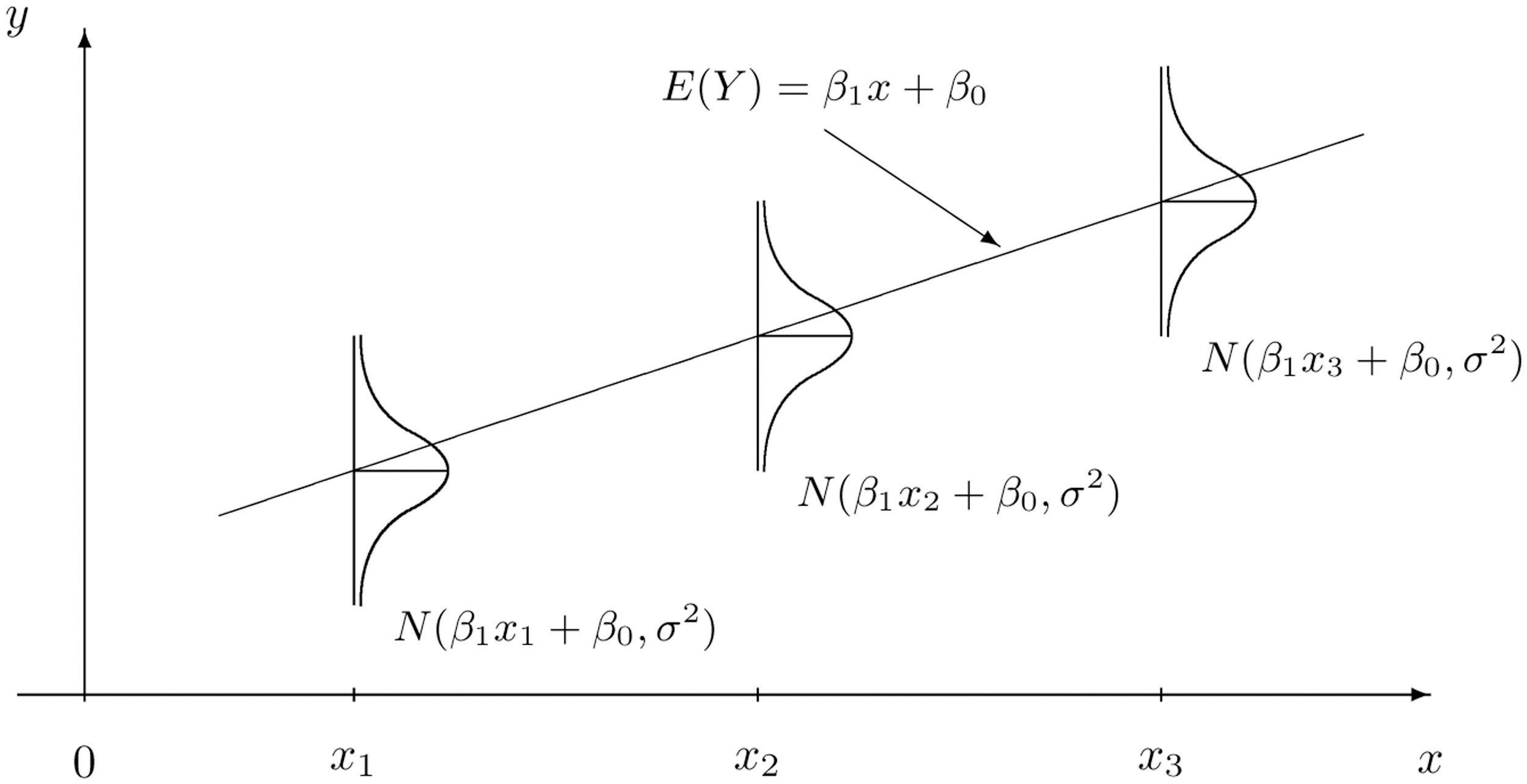

The idea behind SLR

Arsenic experiment example

Is linear regression reasonable here?

Is linear regression reasonable here?

Concept of LS estimation

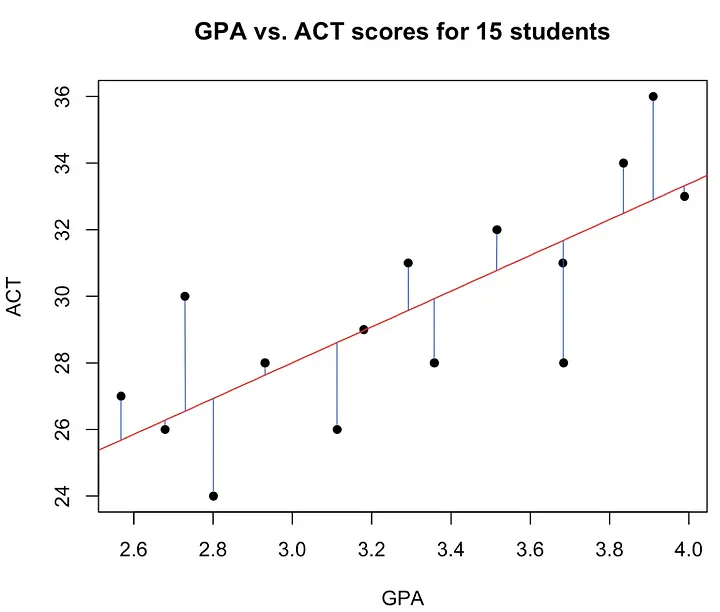

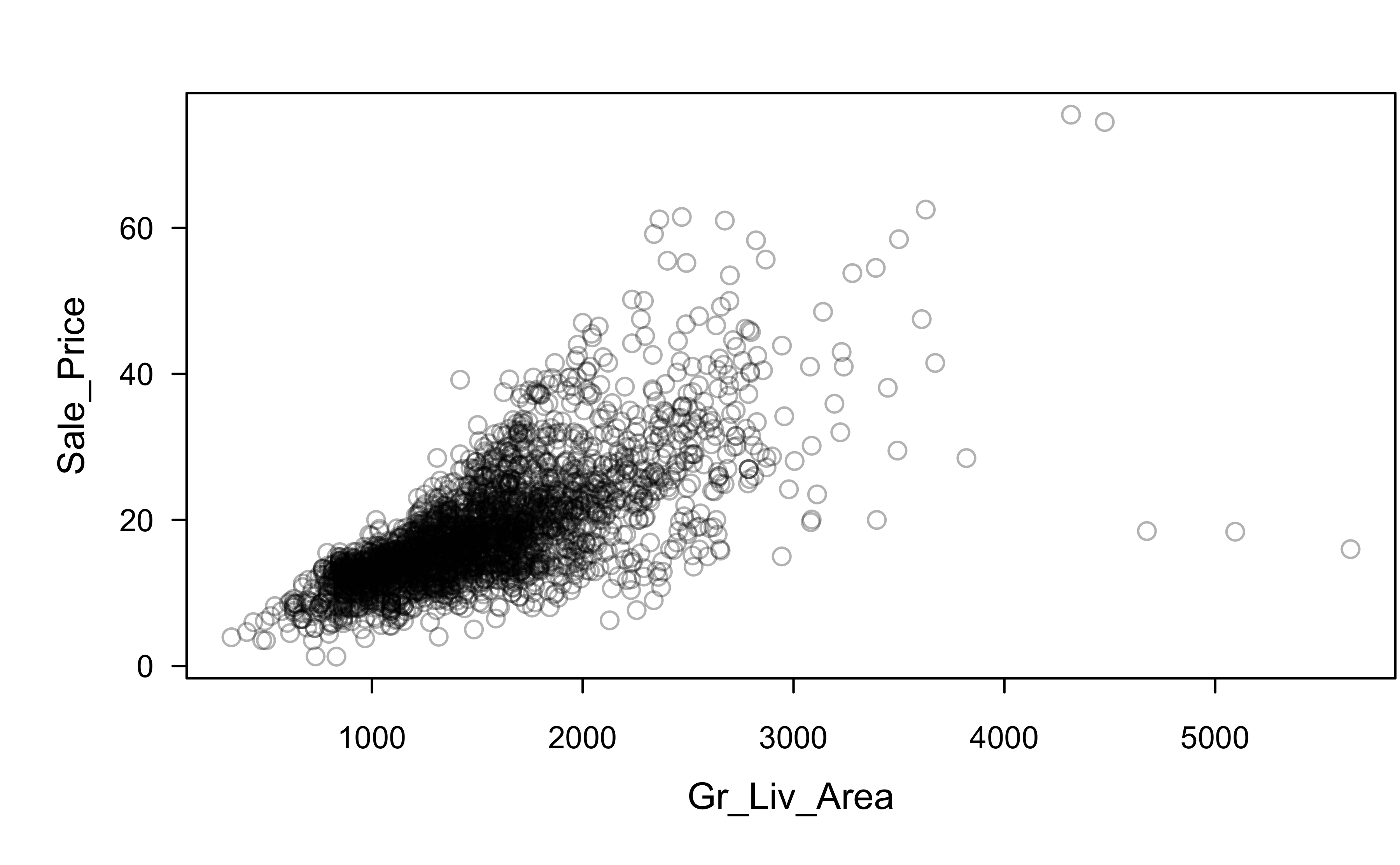

Sale_Price and Gr_Liv_Area

Is this a good fit?

Which assumptions seem violated to some degree?

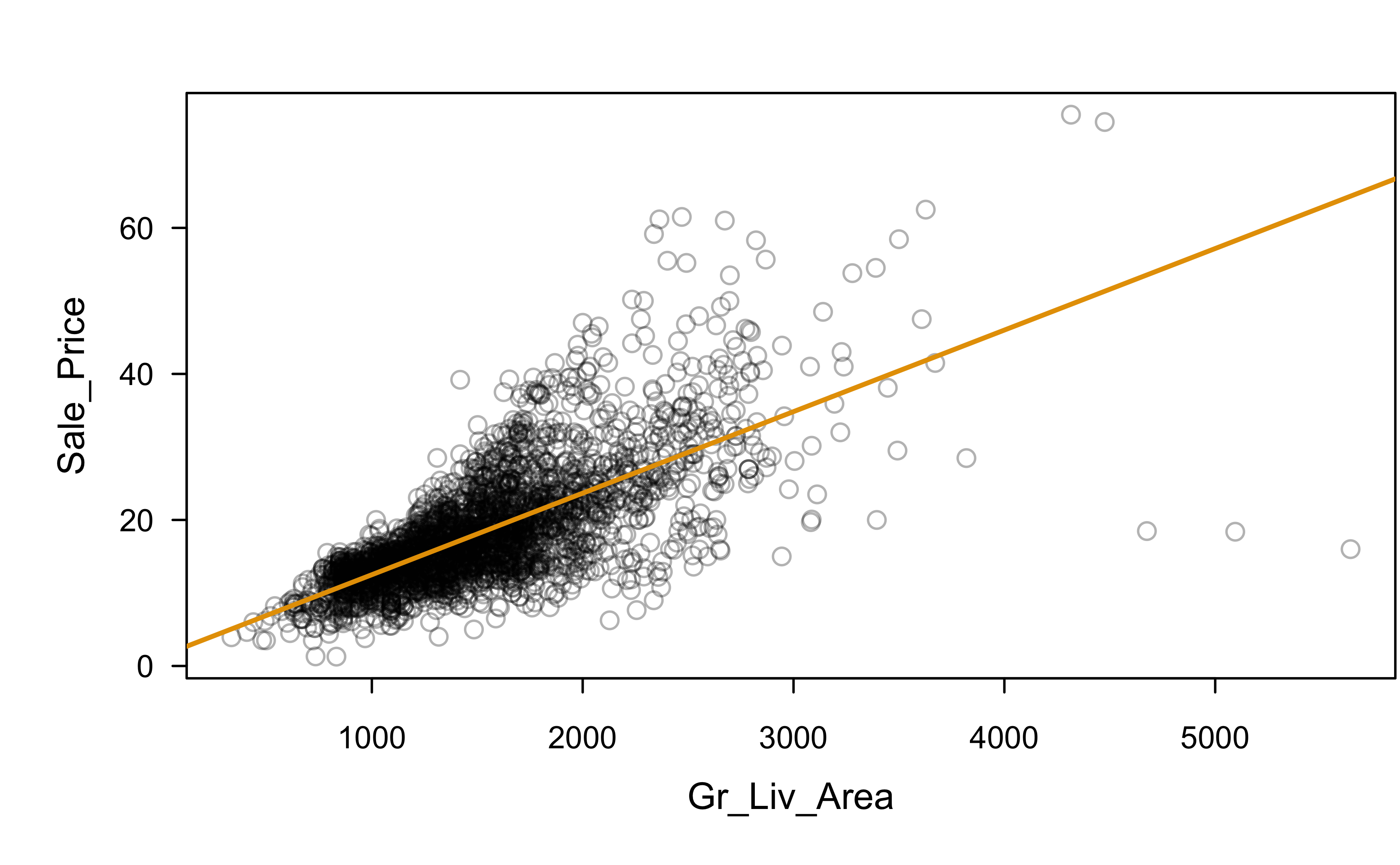

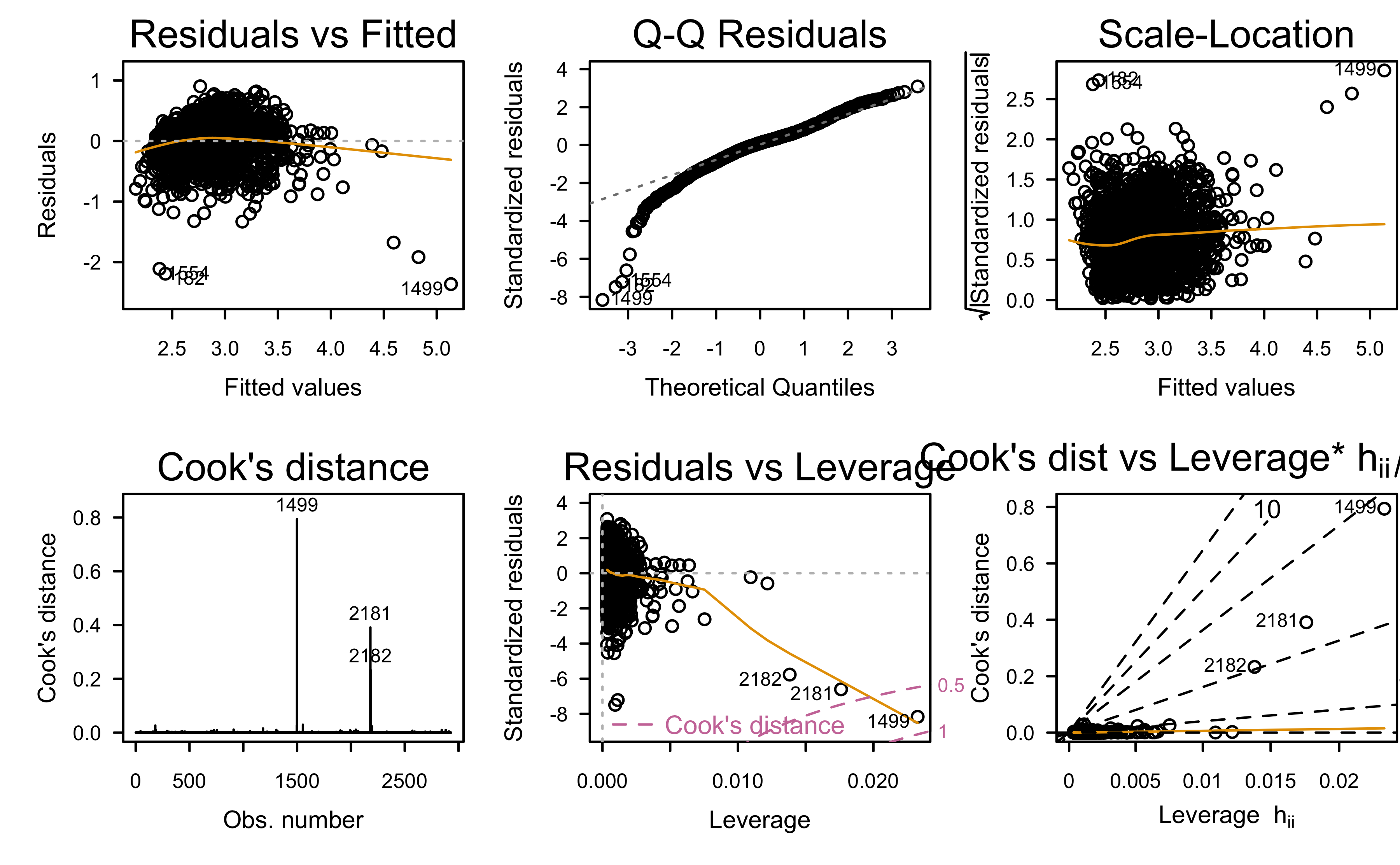

Sale_Price ~ Gr_Liv_Area

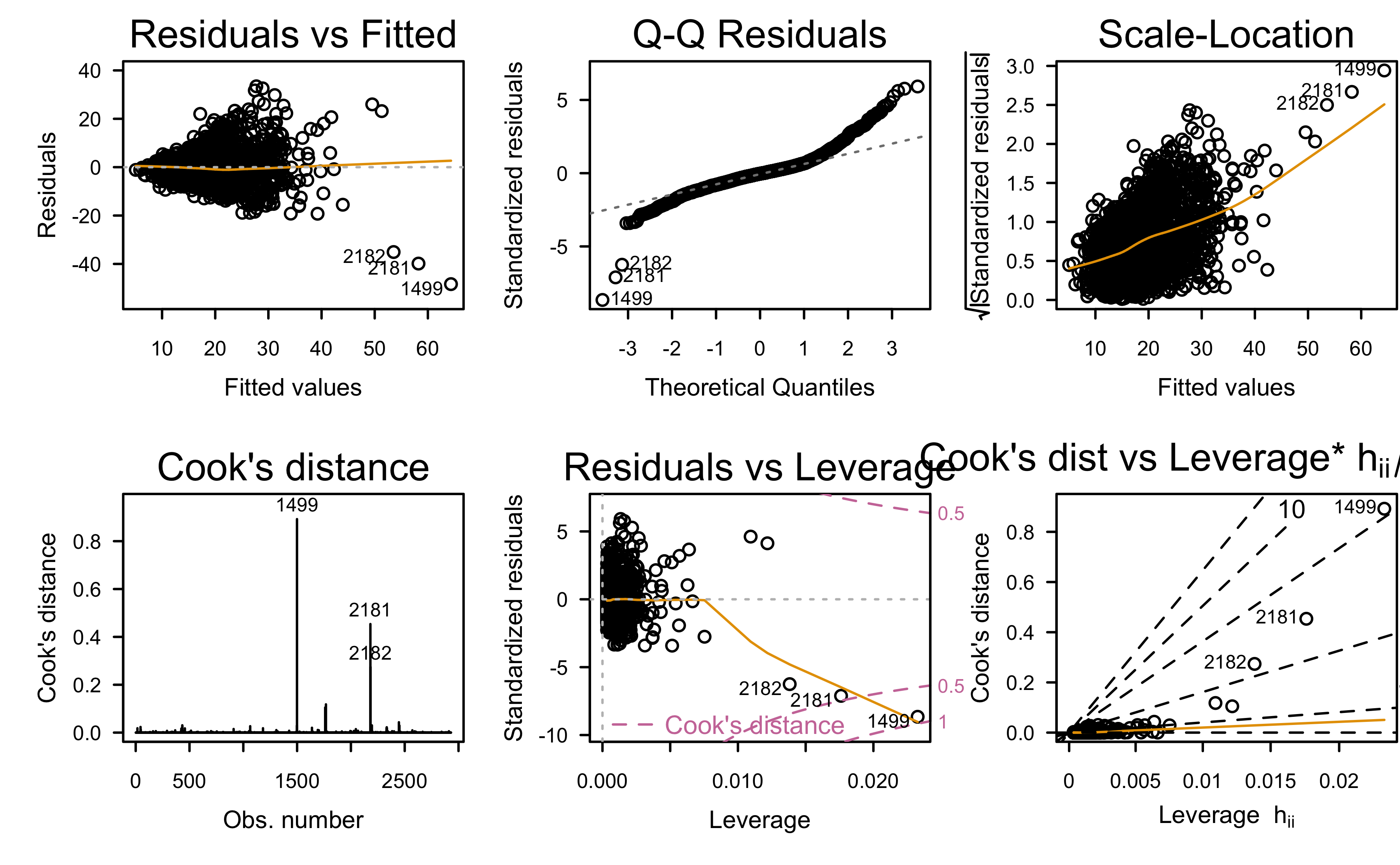

Residual analysis:

What assumptions appear to be in violation?

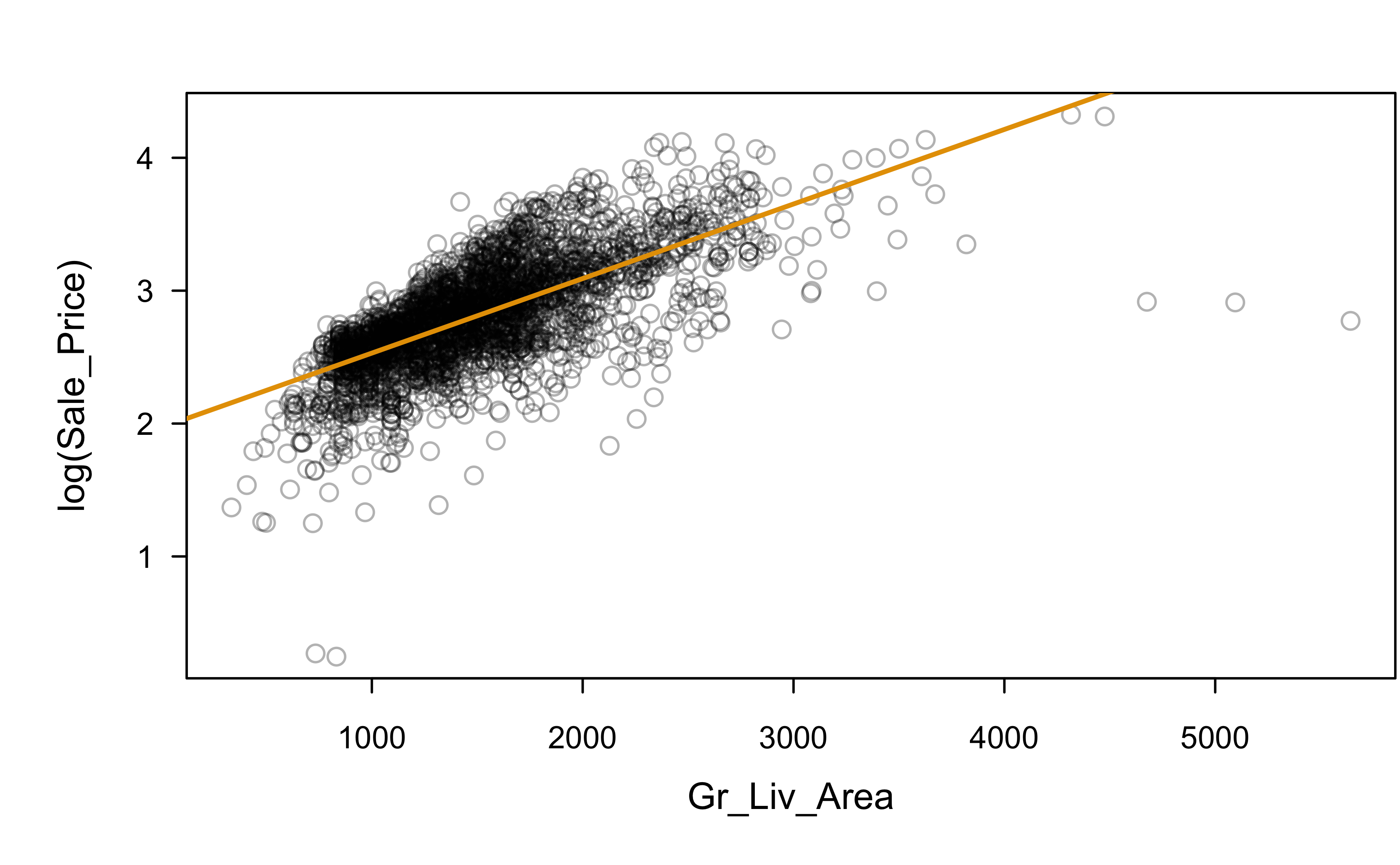

Let’s try a log transformation

log(Sale_Price) ~ Gr_Liv_Area

Residual analysis:

Any better?

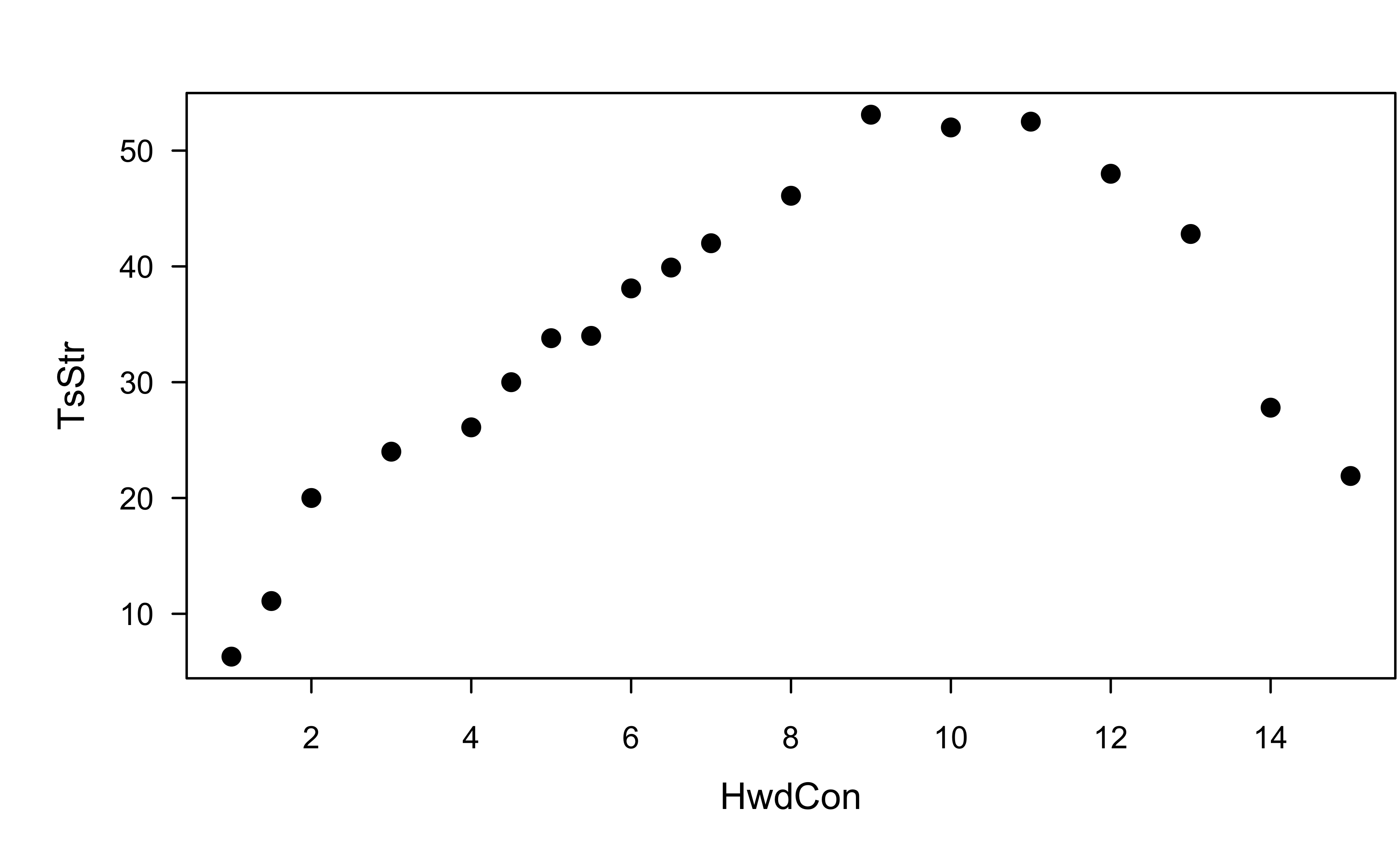

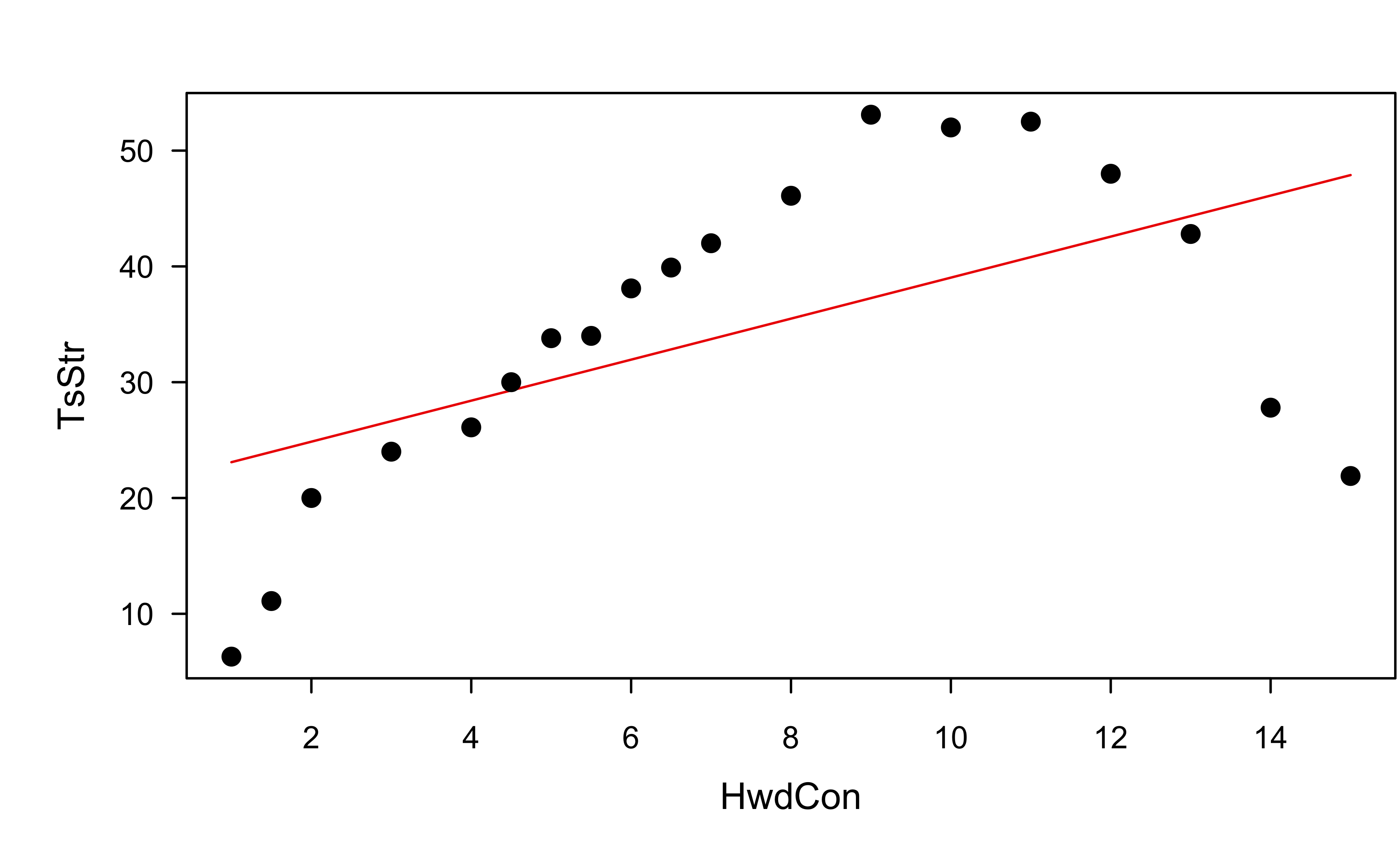

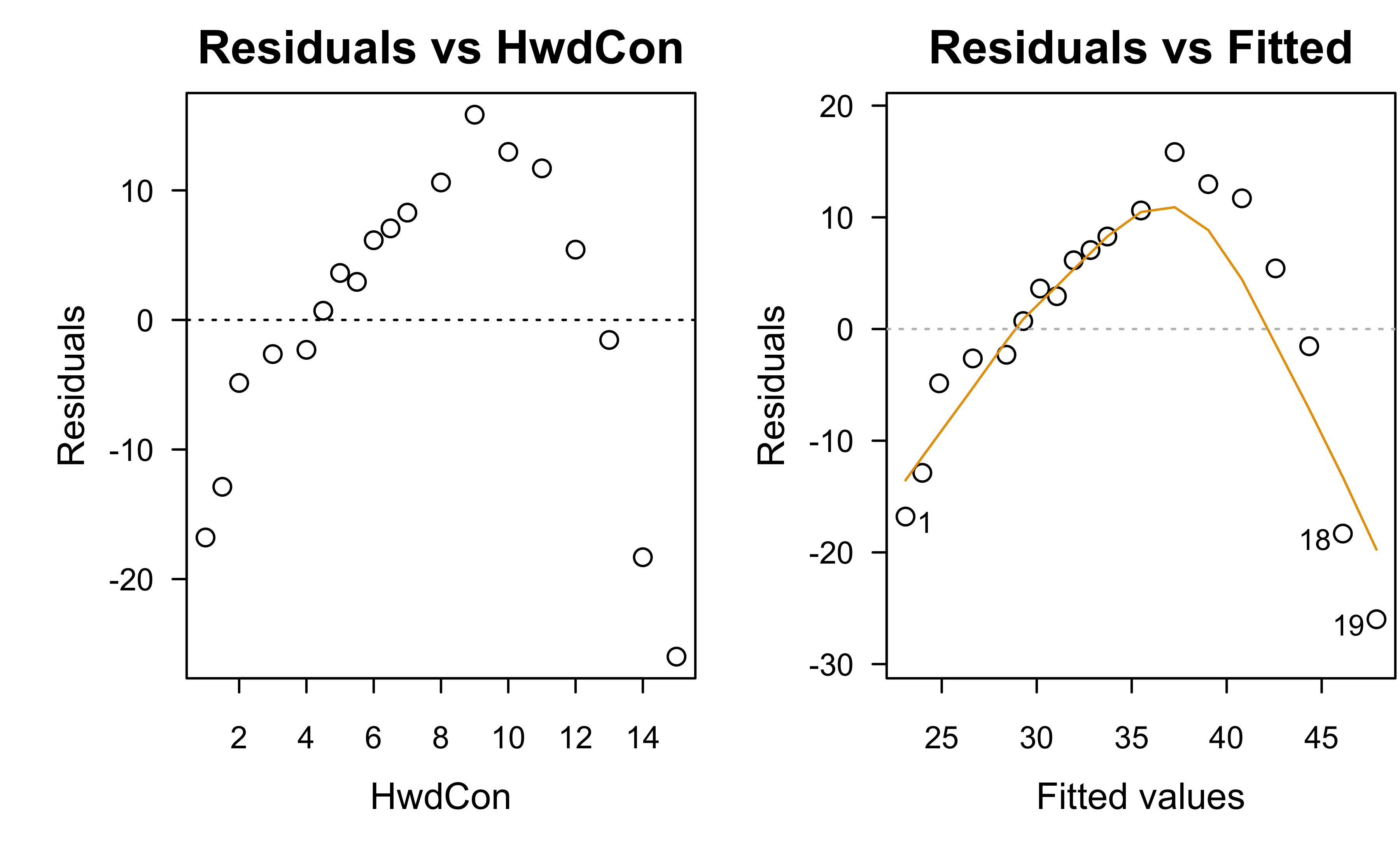

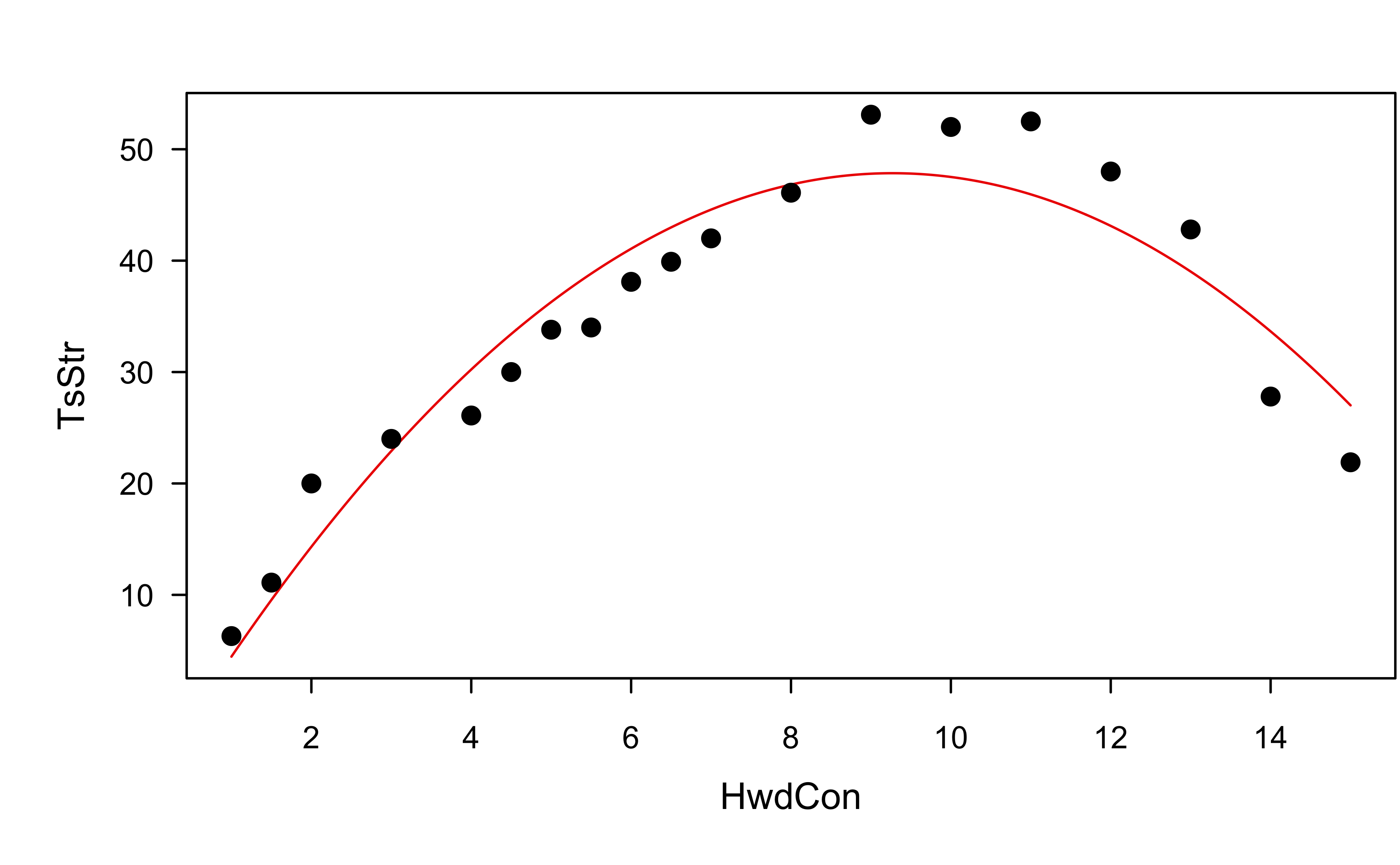

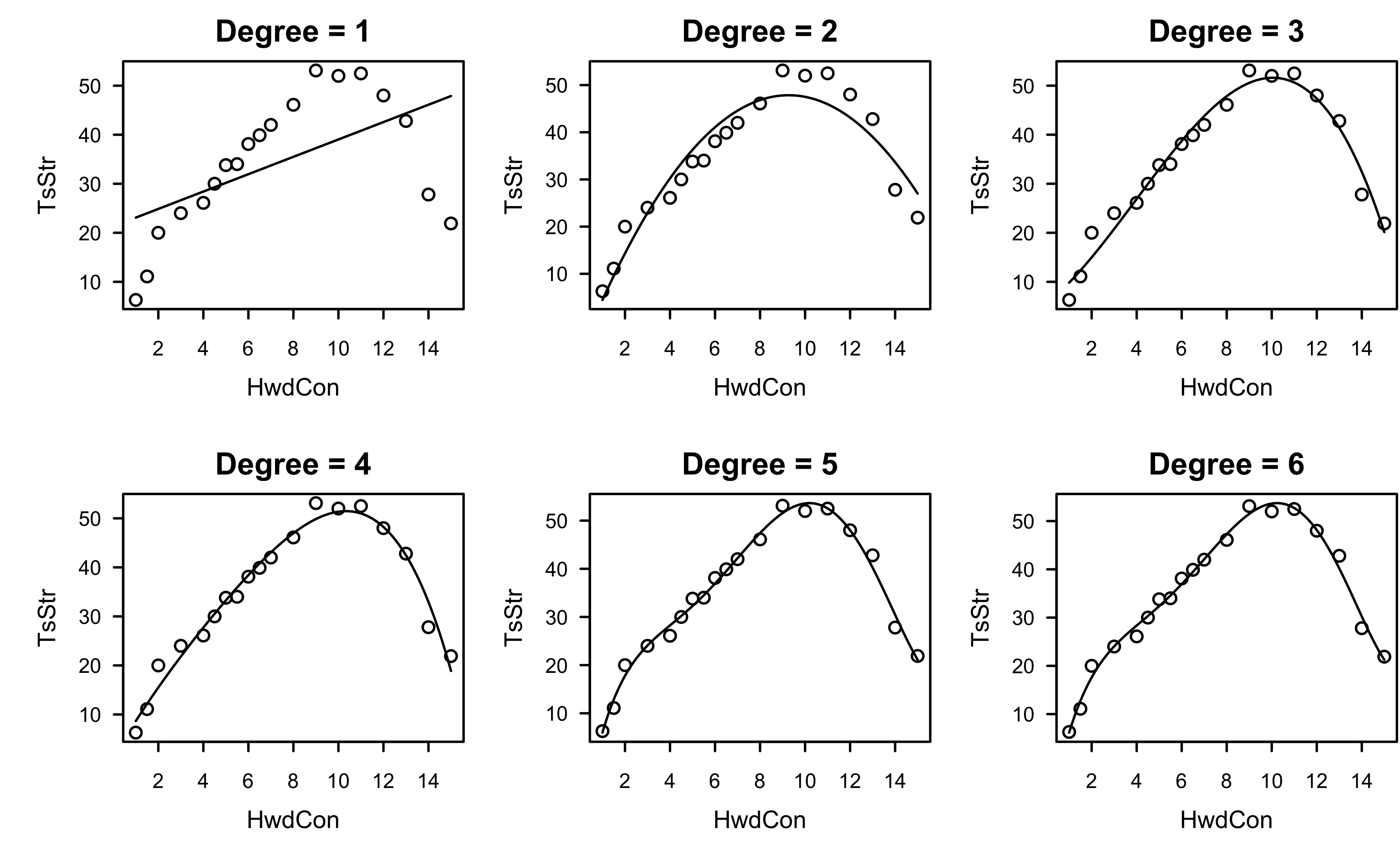

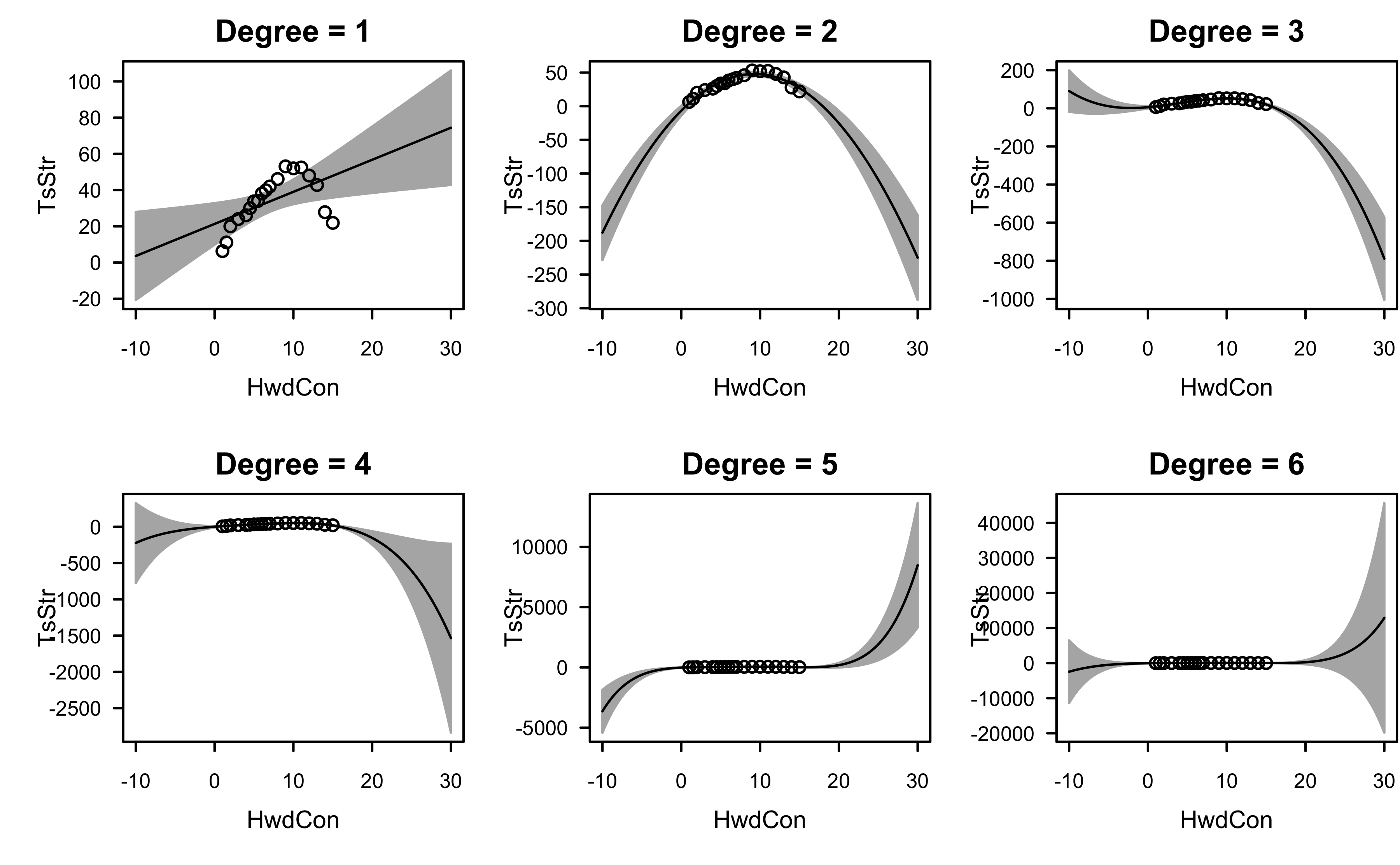

Example: paper strength data

Example: paper strength data

Example: paper strength data

Show R code

Example: paper strength data

Example: paper strength data

Example: paper strength data

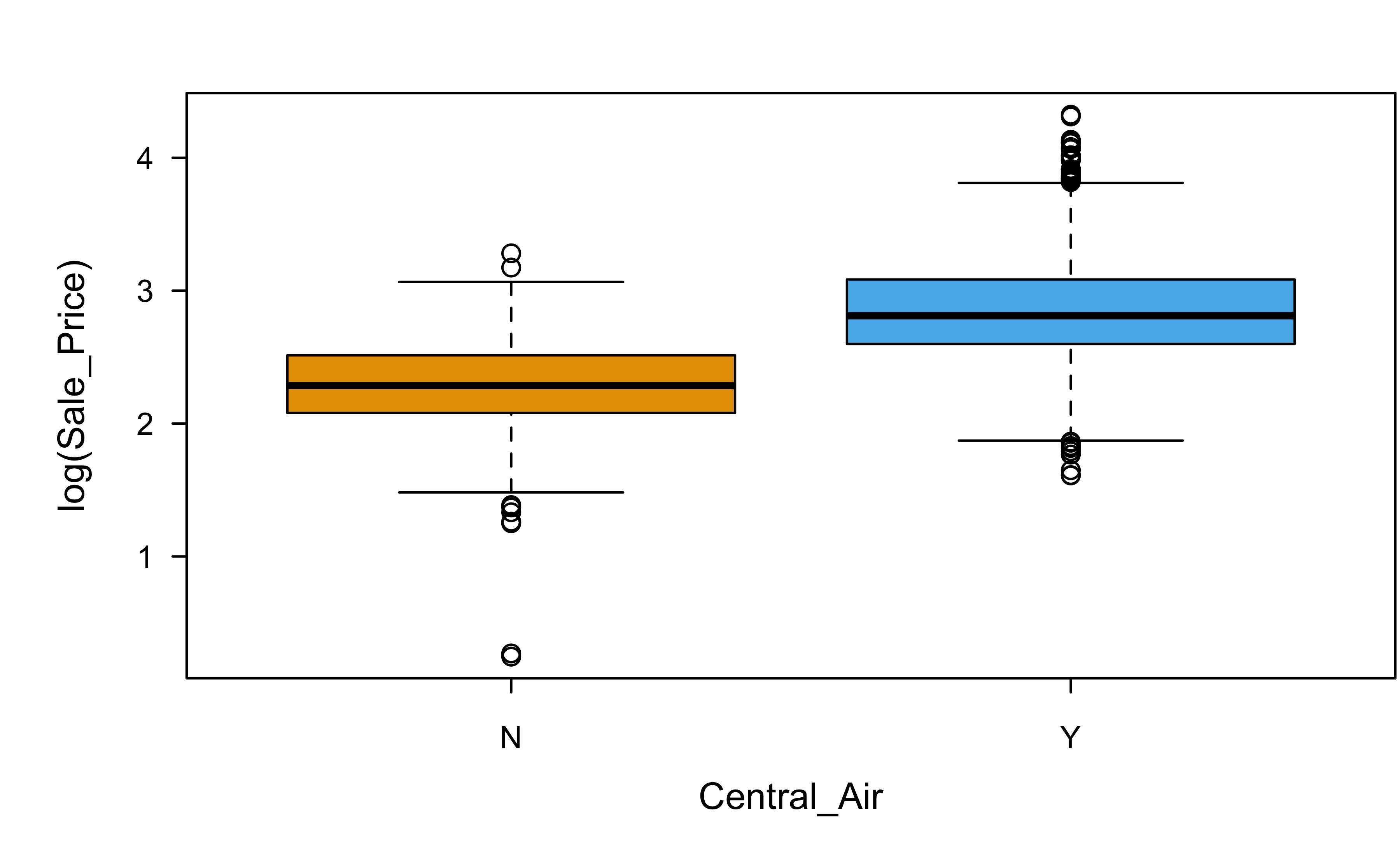

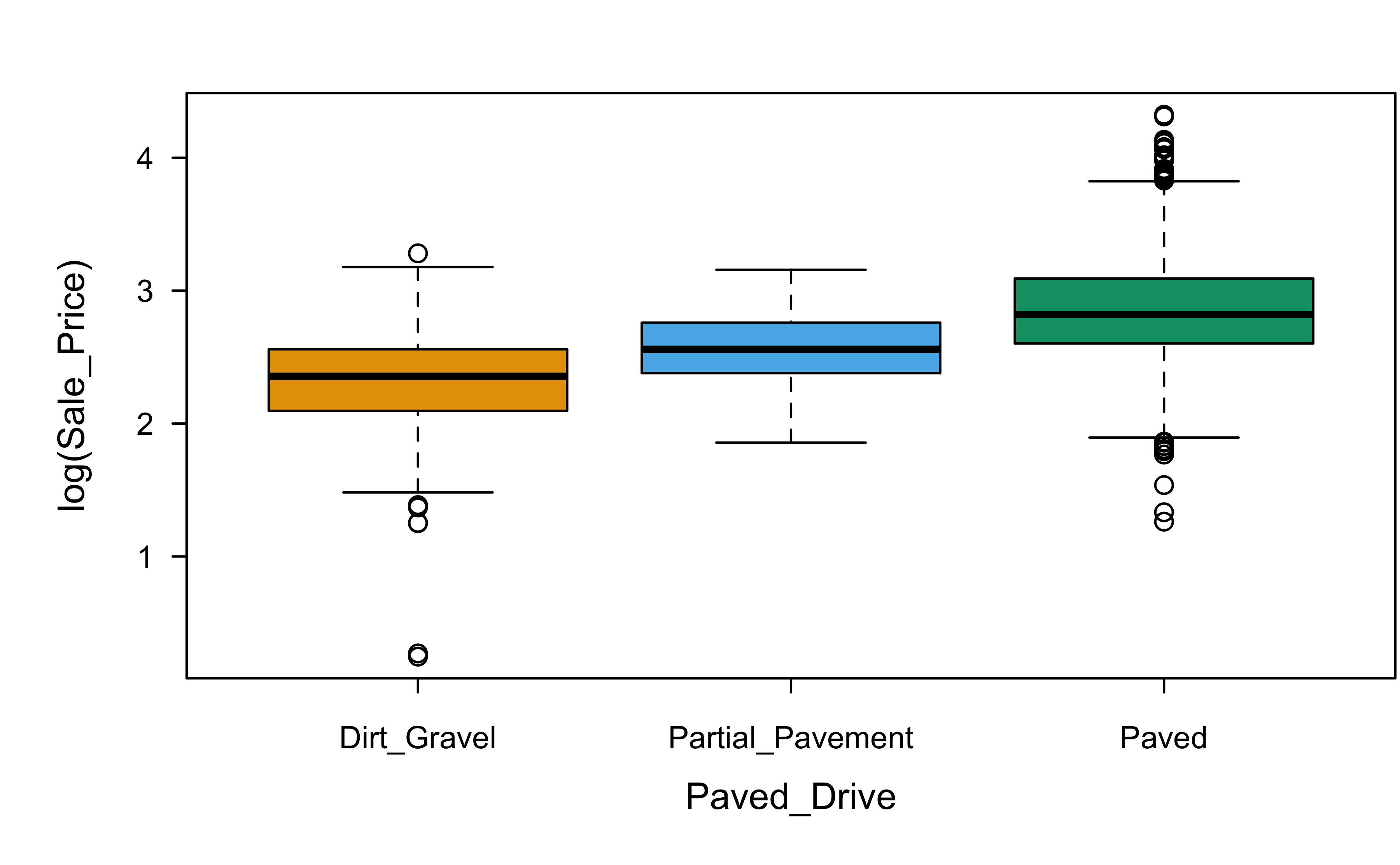

Categorical variables

Categorical variables

If one of these homes downgraded from a paved driveway to a gravel driveway, would that cause the sale price to decrease? (Think very carefully here!)

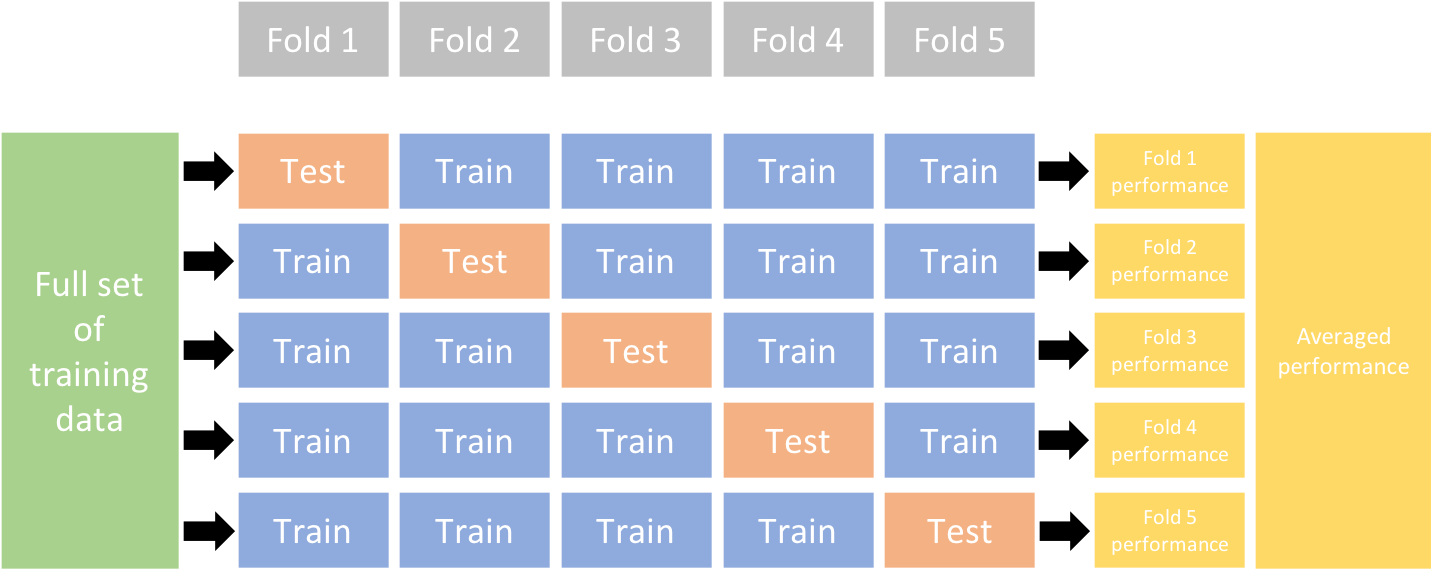

Data splitting: \(k\)-fold cross-validation

The PRESS statistic in linear regression is a special case (\(k = n\)) we get for free!