Linear Regression

A Brief Review

About me

Statistical relationships

Show R code

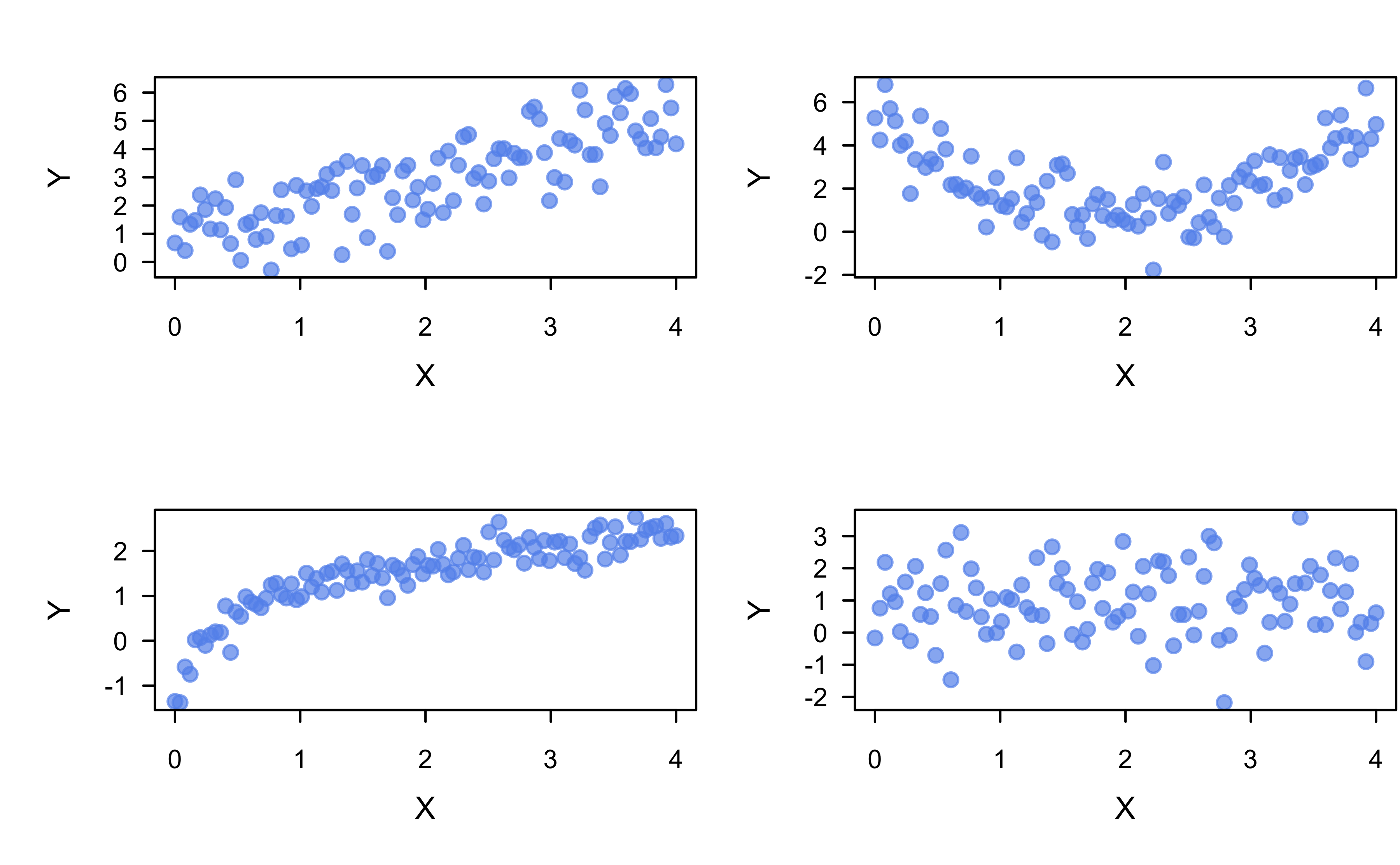

# Simulate data from different SLR models

set.seed(101) # for reproducibility

x <- seq(from = 0, to = 4, length = 100)

y <- cbind(

1 + x + rnorm(length(x)), # linear

1 + (x - 2)^2 + rnorm(length(x)), # quadratic

1 + log(x + 0.1) + rnorm(length(x), sd = 0.3), # logarithmic

1 + rnorm(length(x)) # no association

)

# Scatterplot of X vs. each Y in a 2-by-2 grid

par(mfrow = c(2, 2))

for (i in 1:4) {

plot(x, y[, i], col = adjustcolor("cornflowerblue", alpha.f = 0.7),

pch = 19, xlab = "X", ylab = "Y")

}

Are \(x\) and \(y\) correlated?

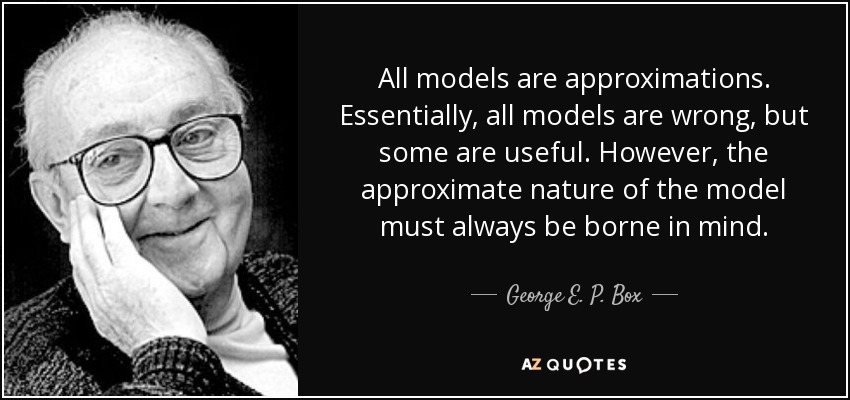

All models are wrong!

Also, see this talk by my old adviser, Thad Tarpey: “All Models are Right… most are useless.”

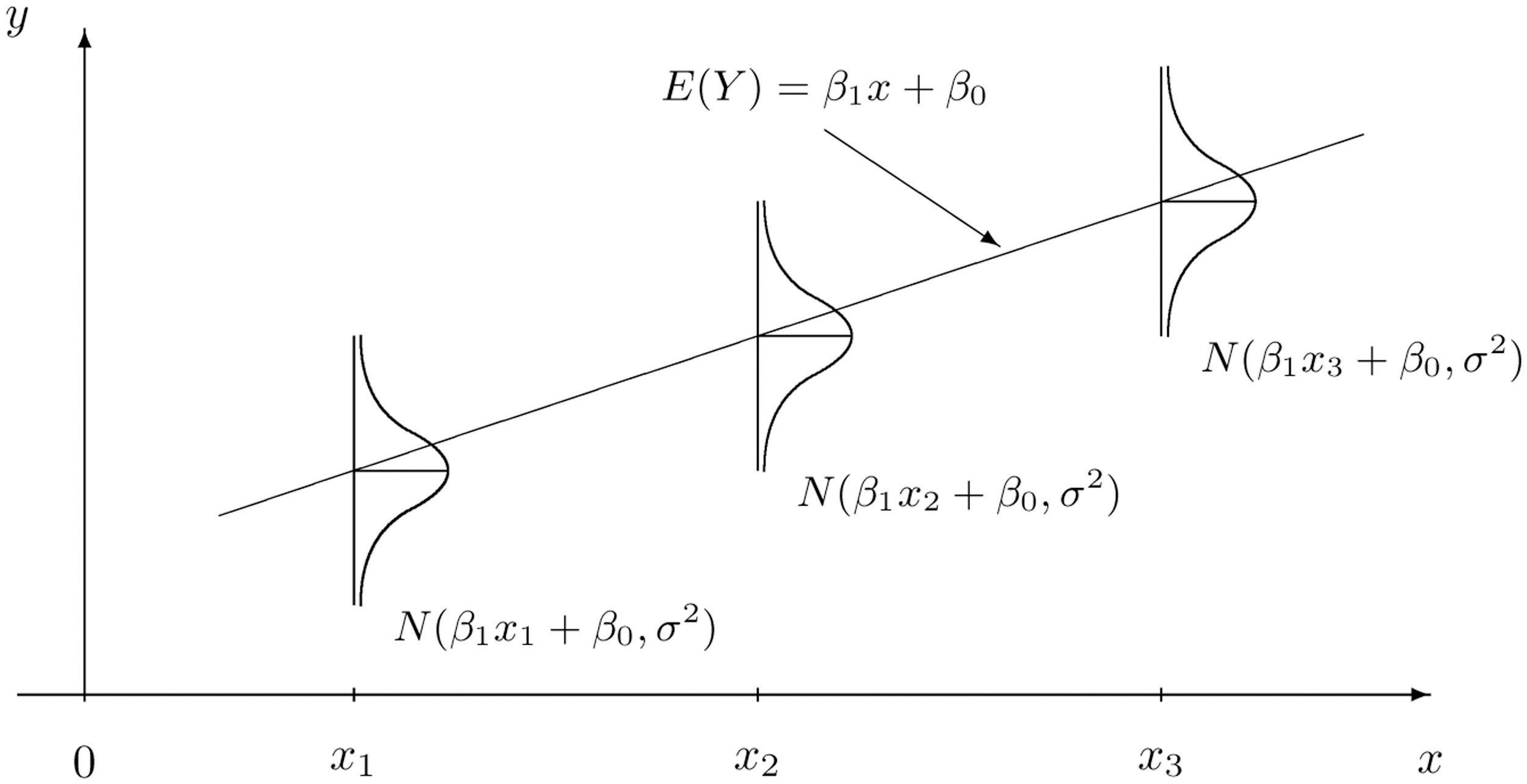

The idea behind SLR

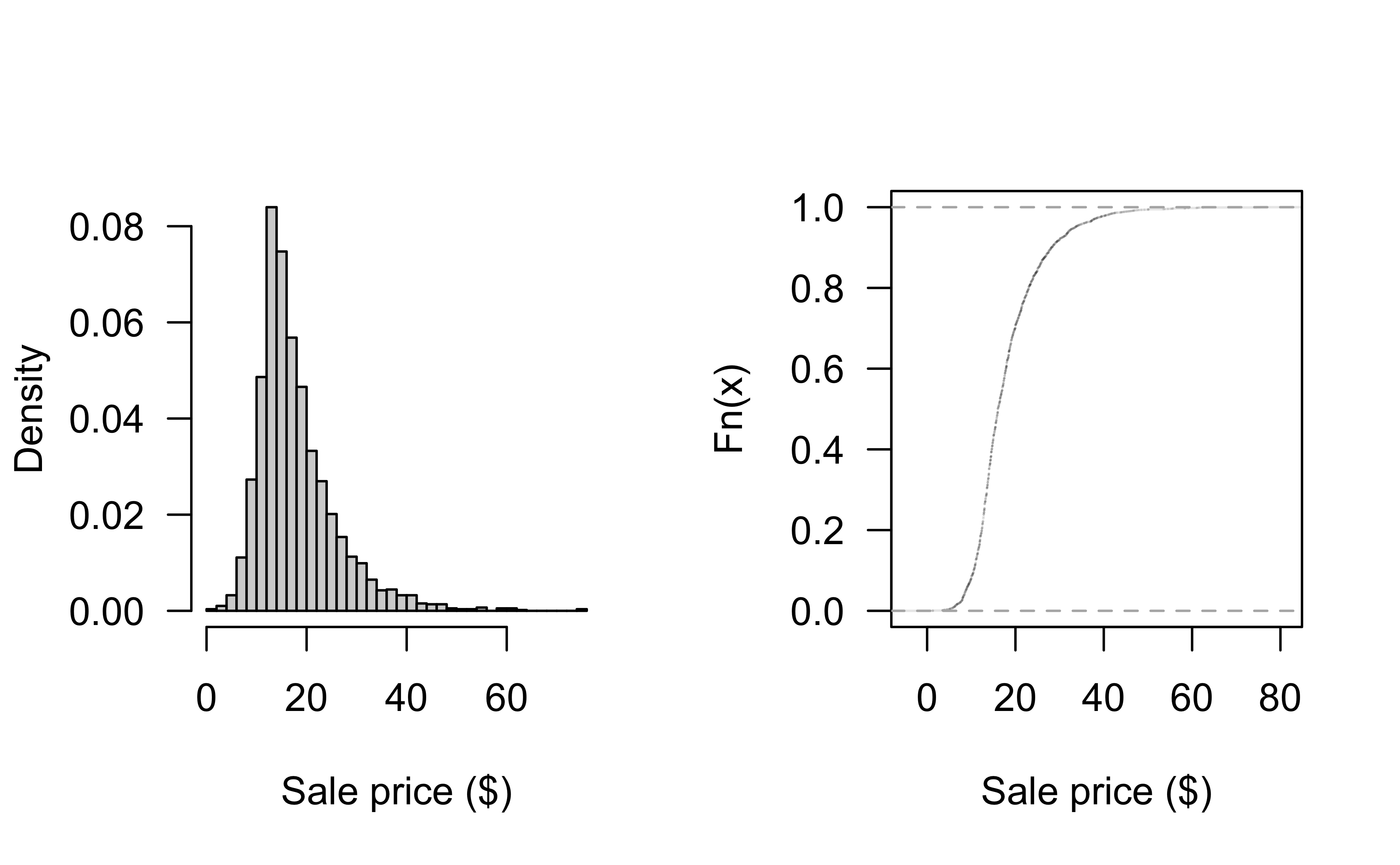

Distribution of Sale_Price

Can look at historgram and empirical CDF:

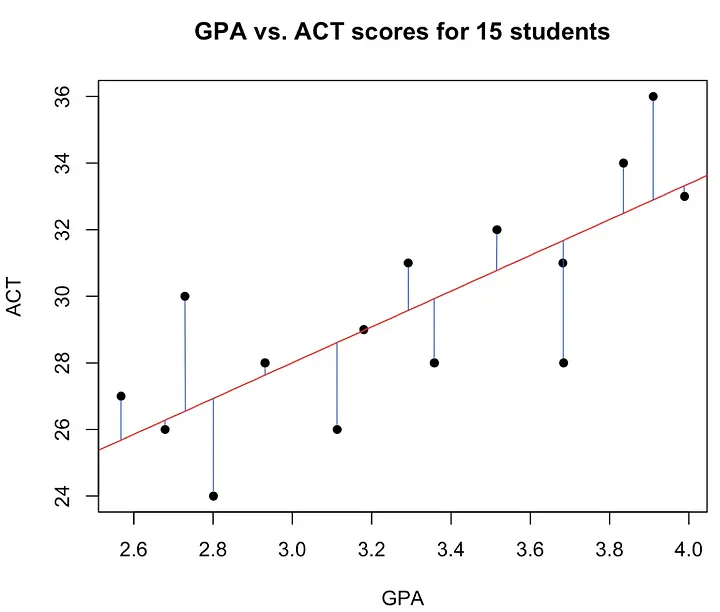

Concept of LS estimation

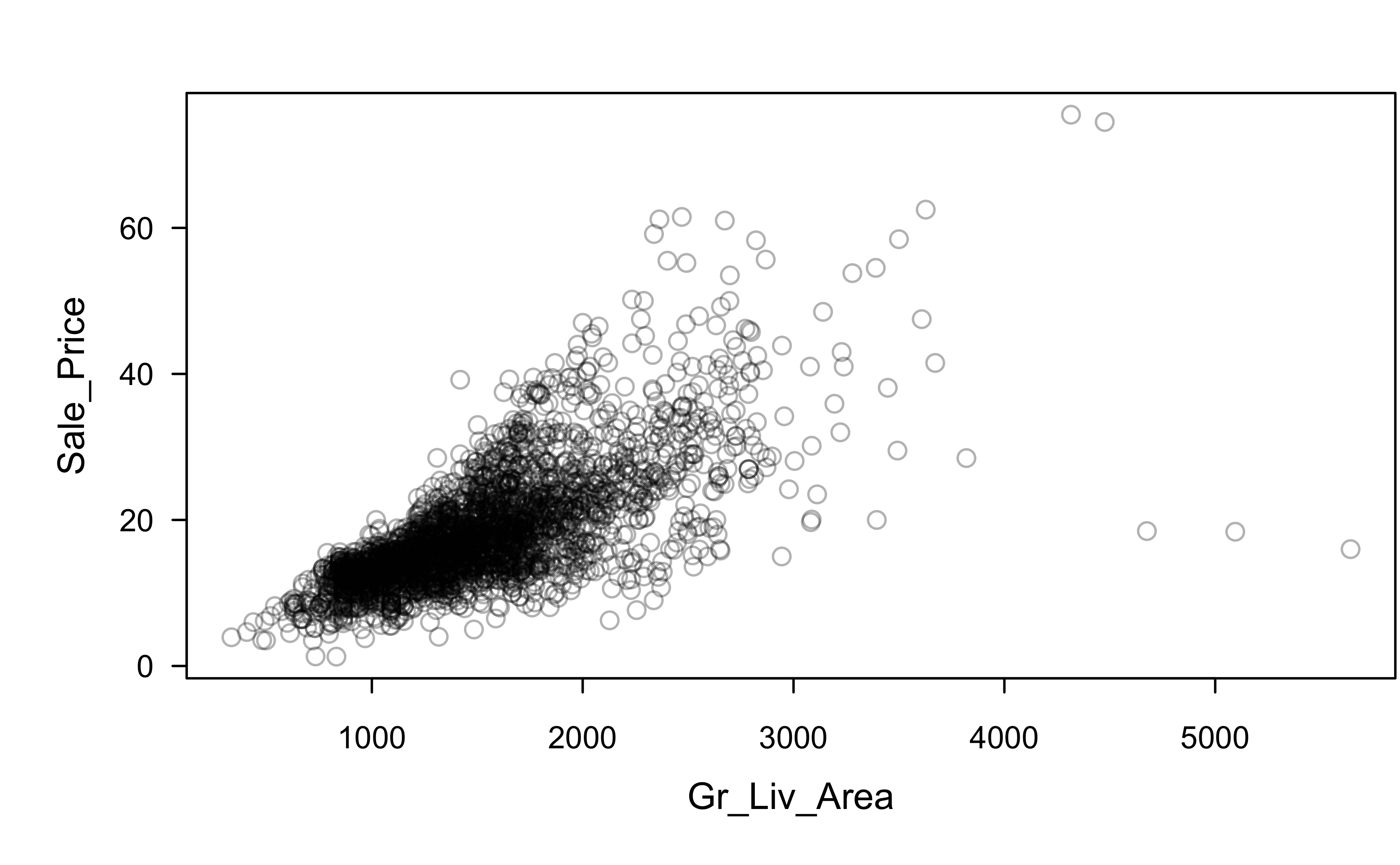

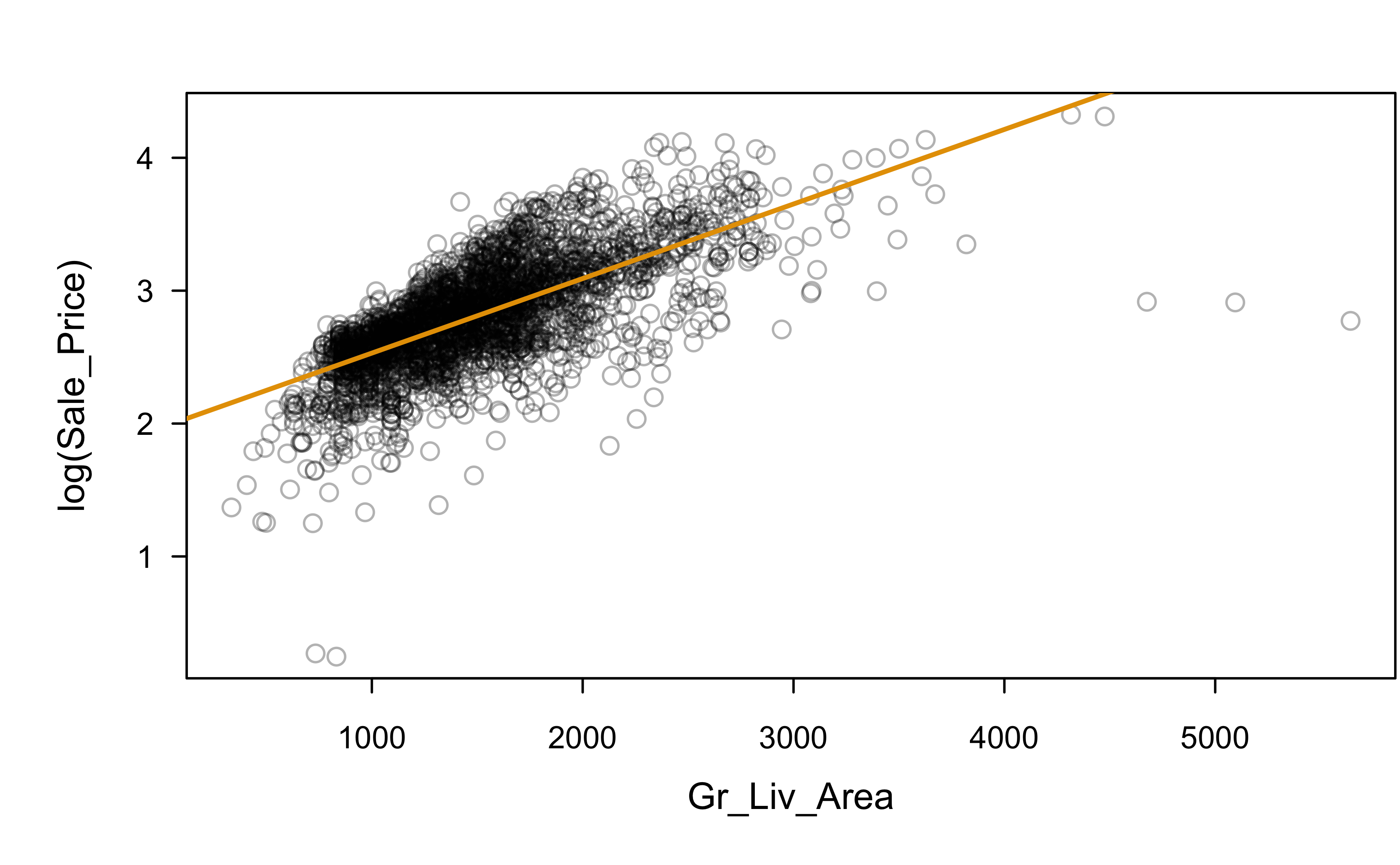

Sale_Price and Gr_Liv_Area

Is this a good fit?

Which assumptions seem violated to some degree?

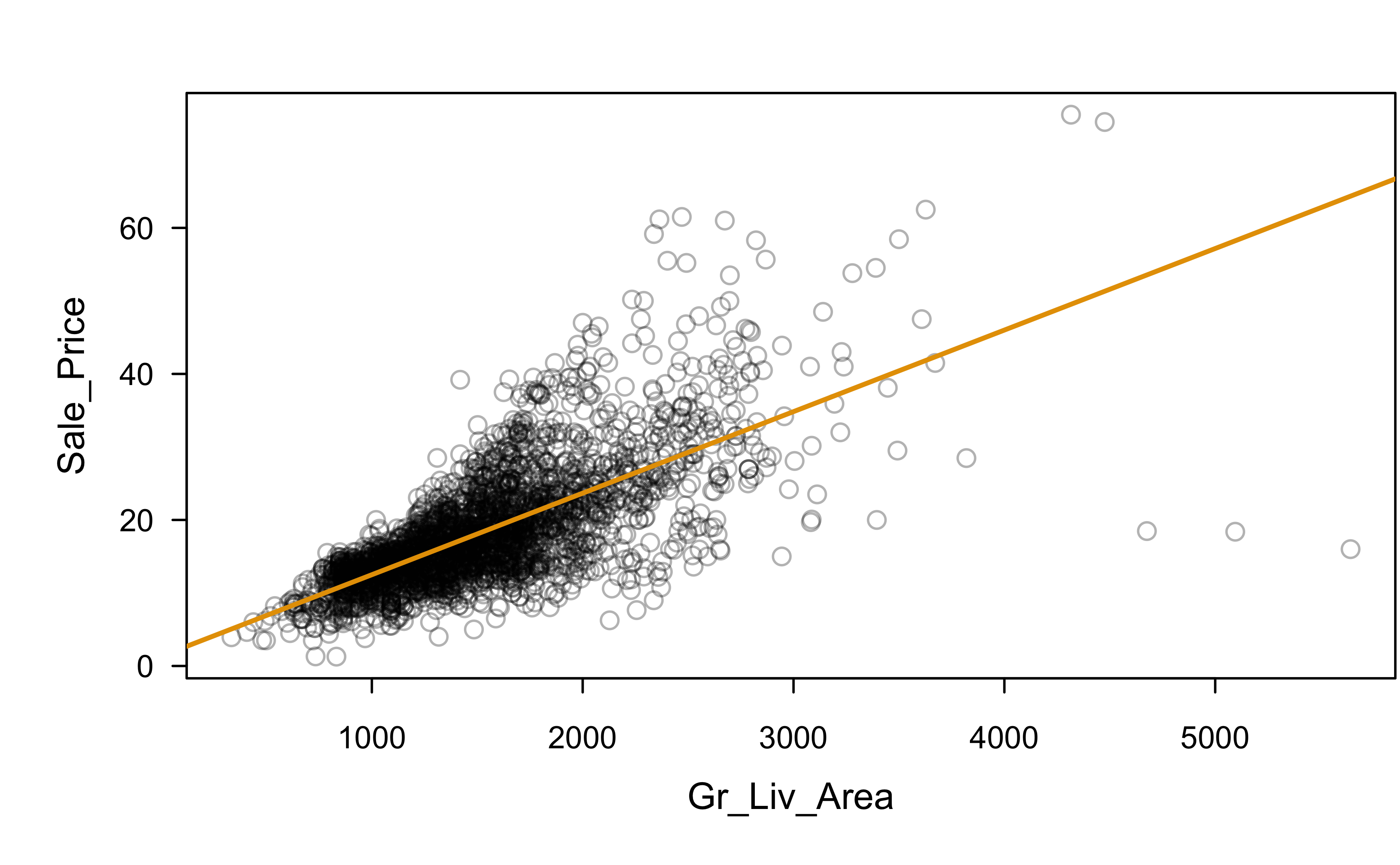

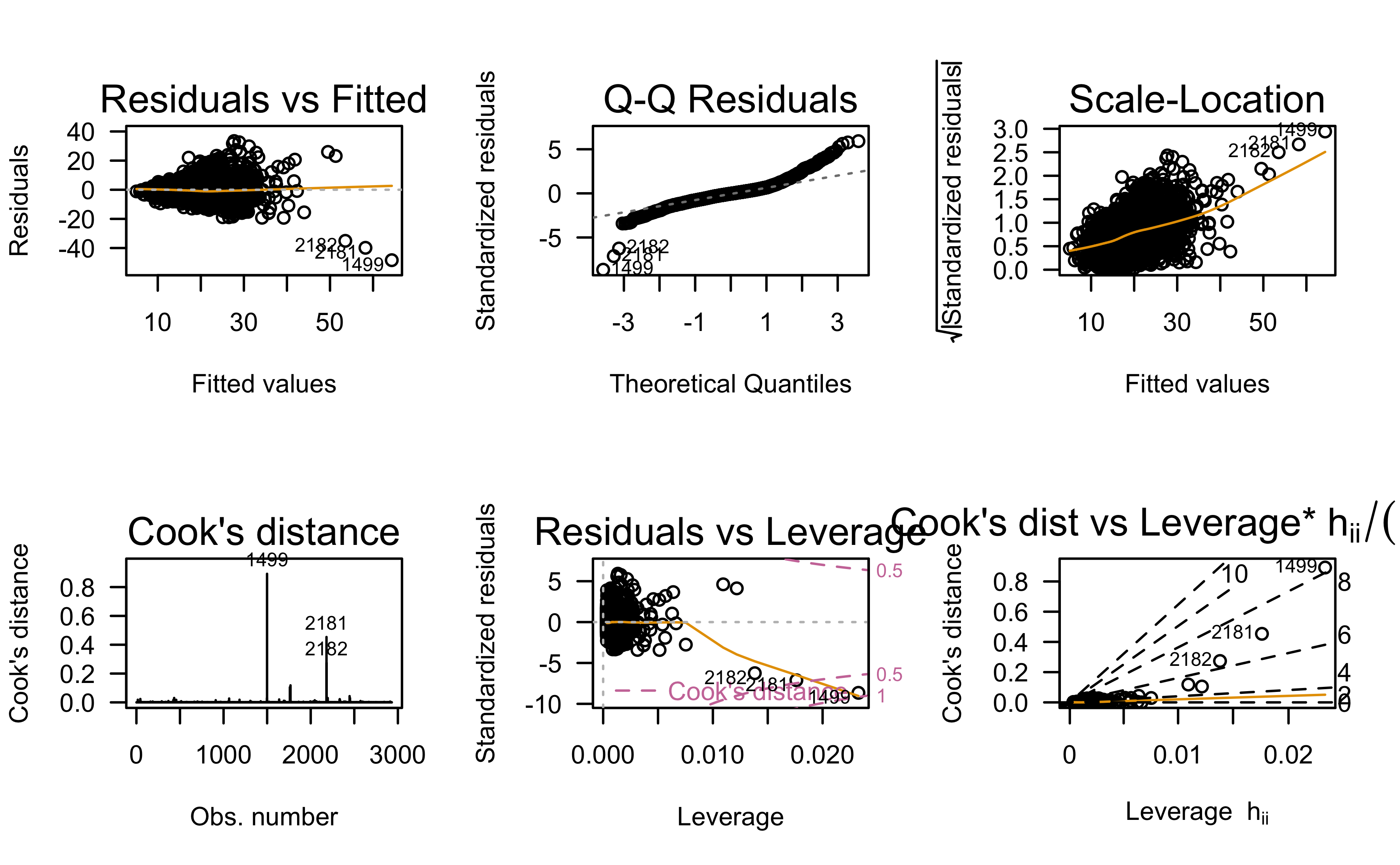

Sale_Price ~ Gr_Liv_Area

Residual analysis:

What assumptions appear to be in violation?

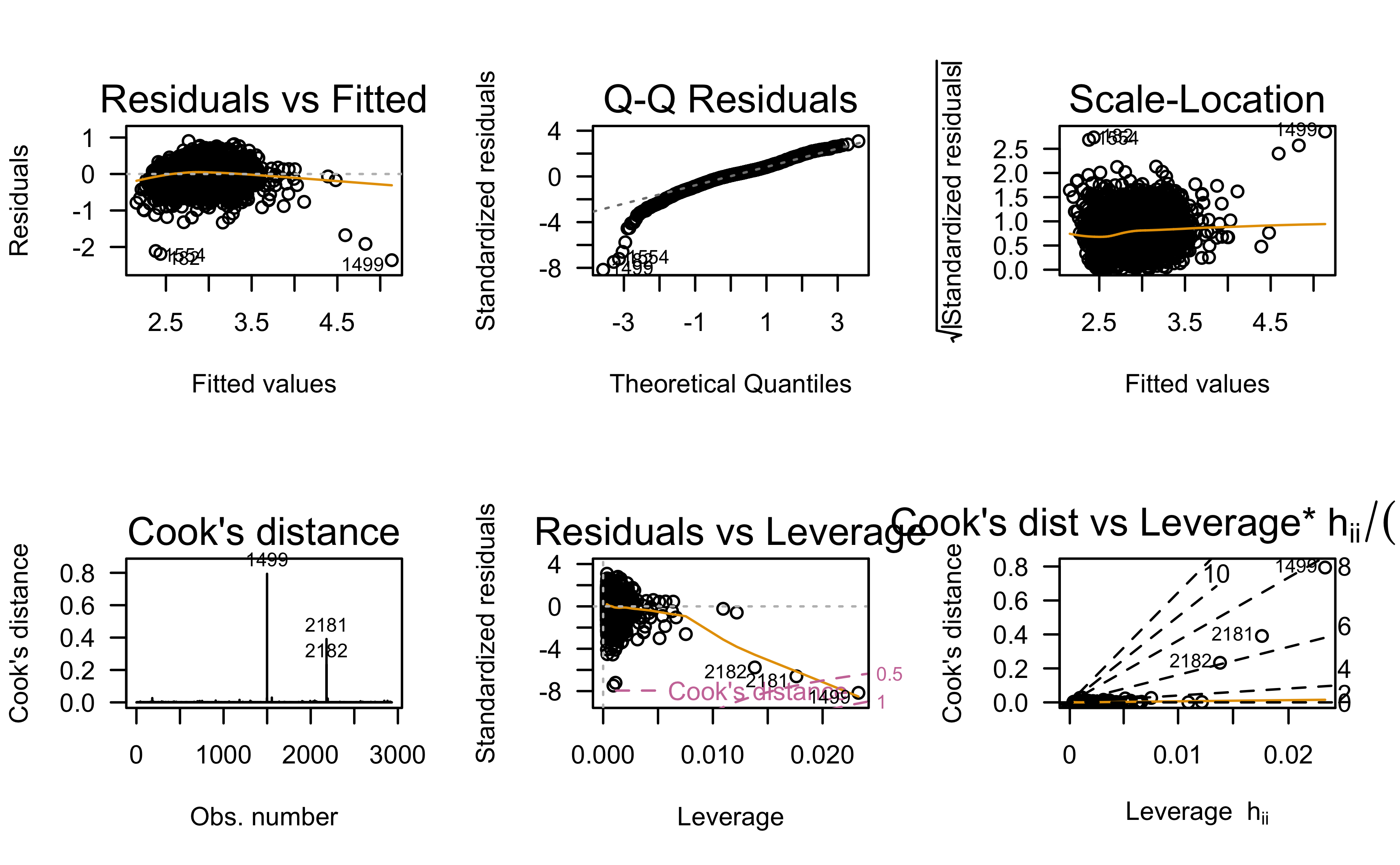

Let’s try a log transformation

log(Sale_Price) ~ Gr_Liv_Area

Residual analysis:

Any better?

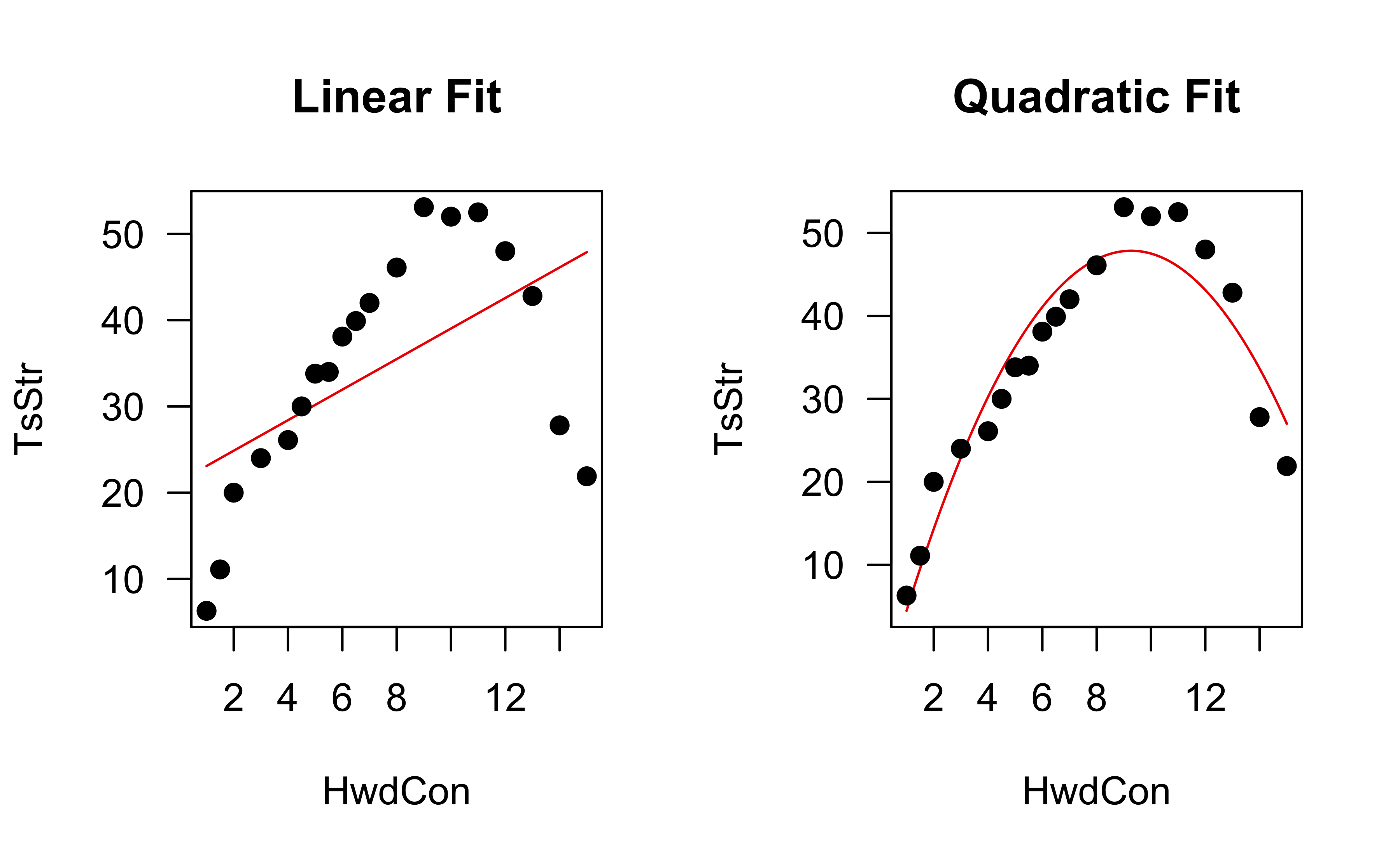

Example: paper strength data

Data concerning the strength of kraft paper and the percentage of hardwood in the batch of pulp from which the paper was produced.